The S&P 500 has retreated from all-time highs as the promise of a US China trade agreement has withered. Additionally, threatened tariffs against Mexico and new troubles with North Korea are weighing on the market. Recent extreme weather threatens to raise US agricultural prices which, in combination with continued and new tariffs, could reverse the benign inflation environment that has helped to elevate asset prices in recent years.

{kind=link}

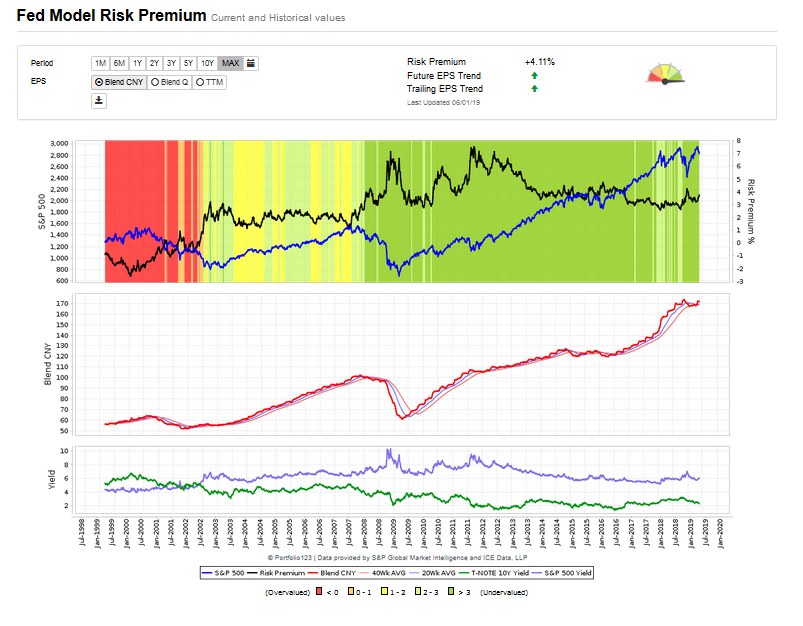

US equity market prices are not expensive as measured by the current 4.11% Fed Model Risk Premium. This Risk Premium shows that the 6.24% earnings yield of the S&P 500 exceeds the 2.14% yield of the 10-year US Treasury Note by 4.11%. This means the market pays equity investors an additional 4.11% to buy the S&P 500 over the 10-year US Treasury Note yield.

Below is a composite of charts showing the components of Fed Model Risk Premium. The top chart shows the Risk Premium since 1998 ranging between -2.6%, at the 2000 peak, and 7.53%, following the financial crisis. The current 4.11% reading is relatively attractive. The middle chart shows earnings estimates. This year’s earlier contraction in earnings estimates has recently reversed reflecting solid economic data and improving corporate forecasts.

{kind=link}

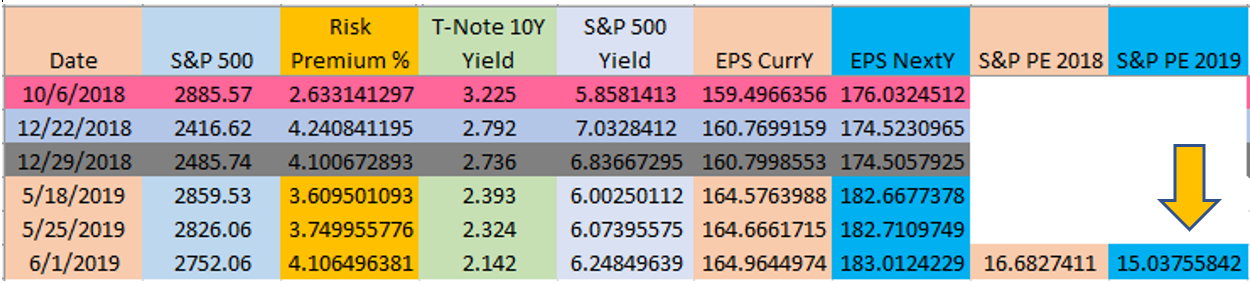

The data box below shows the Risk Premium component values at recent key dates: the market peak last fall, the Christmas eve nadir, year end and May’s end. The S&P 500 is currently priced at 15.04 times 2019 estimated earnings. While not compellingly attractive, the S&P 500 is a good value.

{kind=link}

Since year end the 10-Year Treasury yield has decline 59 basis points, from 2.74% to 2.14% due to a more accommodative Federal Reserve bias, concerns of global economic weakness and recent market fears. This cautious bond market perspective stands in contrast to that the US equity market where high consumer confidence and low employment paint a constructive view of the US economy. This dichotomy of equity and bond market perspectives explains the recent rise in the Risk Premium from 3.22% to 4.11%. This current level is comparable to the year end reading – an excellent entry point for equity investors.

Recent news is concerning, though not frightening. The chart below of the CBOE Volatility Index VIX, shows a rise to an 18.71 reading from the complacent levels which had accompanied April’s equity market highs. This sentiment chart suggests that market fear could rise a good bit more, before equity markets provide a compelling entry point. If President Donald Trump’s negotiating brinksmanship matches his professional career’s bravado, the administration will not back off nard nose negotiations with China, Mexico or North Korea any time soon. Consequently, we should expect several months of geopolitical fireworks. However, by October, the President might shift his attention to the 2020 Presidential election and begin softening the administrations’ tough negotiating positions. Should a compromising negotiating tone and agreement(S) ensue, then, a market rally, coincident with the Presidential campaign would stand to reason. Not to suggest politics could be Machiavellian, but since the VIX peaked at 36 at the market low on Christmas eve–when the market misinterpreted a tweet by Secretary Treasurer Steve Mnuchin– one could argue that market fears could worsen appreciably from current levels before the administration’s geopolitical brinksmanship jeopardizes the US economy, equity market and Trump Administrations reelection prospects.

{kind=link}

The most important pending global economic event remains the US China trade negotiations. If the United States is able to stop or significantly curtail the systematic theft of American intellectual property and forced technology transfers, the prospect for a more durable economic cycle improves markedly. With China’s recent rejection of key negotiated trade concessions, it could be several months until both countries can find a political face-saving and substantive compromise. With the US economy larger and stronger, the administration is not likely to capitulate soon. Since the long-term secular growth implications of a reversal of China’s predatory and opportunistic trade practices are so significant, it would not be surprising to see this negotiation extend several more months.

“Project Harpoon”: ArcLight’s problematic Acquisition of American Midstream Partners, LP

When a fairness opinion references “Project Harpoon”, one cannot help but wonder if someone has a sick sense of humor and American Midstream Unit holders are getting a raw deal.

{kind=link}

A Brief History of Acquisition:

- American Midstream and its common units (AMID) were aggressively recommended by AMID’s CEO Lynn Bourdon in the $13/share range in 2017 and 2018.

- Lynn Bourdon also stated definitively that ArcLight Capital Partners, LLC, (“ArcLight”), a $21 Billion dollar energy Private Equity firm, was a supportive backer of AMID and would be supportive in the future1.

Since ArcLight had provided financial support to AMID to maintain its distribution, there was a reasonable expectation that ArcLight had the interests of AMID unit holders in mind, as investors of publicly traded securities assume management works in their interest. In December 2017, at the Wells Fargo MLP Conference, I met with AMID’s management2 as it had grown to be an outsized position for our customers. (AMID had merged with JP Energy (JPEP) and both positions had appreciated about 100% each since we bought them for our clients during the 2016 oil and MLP market bottom.) Management assured us then and subsequently3, that ArcLight was a supportive sponsor interested in helping AMID unitholders.

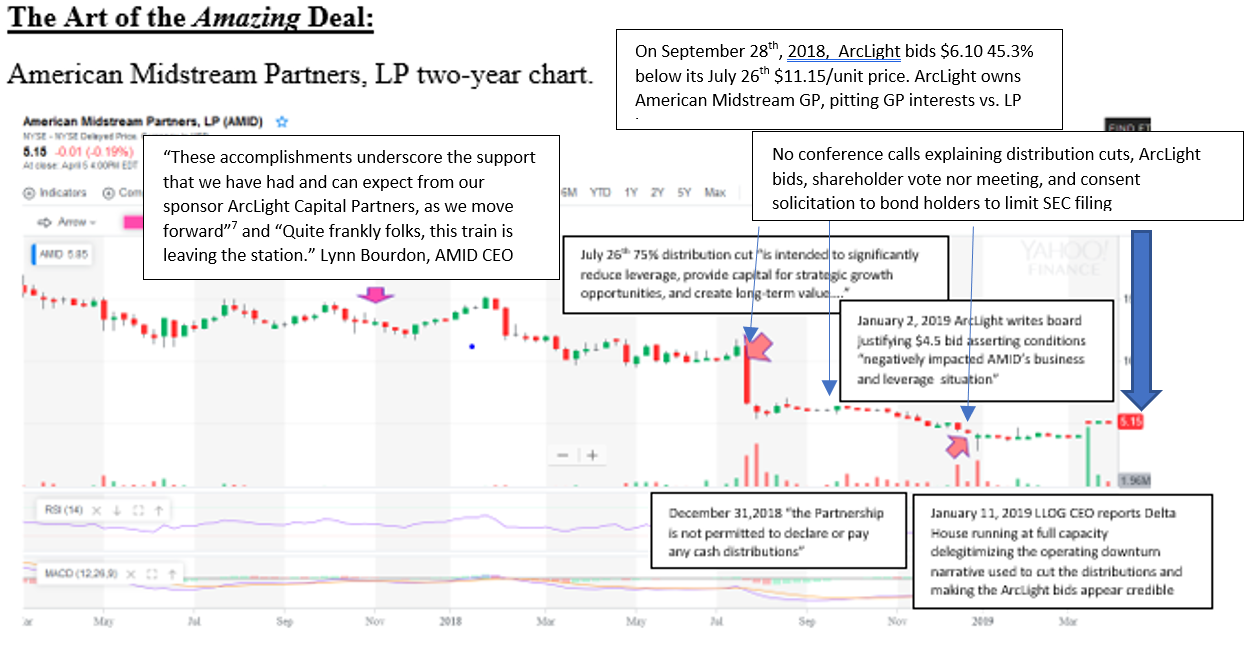

- On the July 26th 2018, AMID announced a 75% distribution cut and new capital allocation strategy. Oddly, management, led by CEO Lynn Bourdon, ceased making regular normal conference calls and Q&A available. On July 27th, AMID units dropped 43% on 20 times average volume.

The absence of a conference call was highly unusual. Most major corporate actions, such as a major distribution cut and or new capital allocation strategy, are followed by a conference call to explain the new corporate action and objectives. AMID did release this announcement.

Three weeks later, after numerous calls to CEO Lynn Bourdon, Lynn Bourdon, Eric Kalamaras and Mark Schuck returned our call. Bourdon explained there were numerous great growth opportunities for AMID and AMID was selling non-core assets and targeting accretive acquisitions. The distribution cut would fund the new investments and expedite the delevering of the balance sheet and they had an $800 million “wedge” they sought to acquire. Long term, this strategy made sense. Therefore, we added to our AMID position.

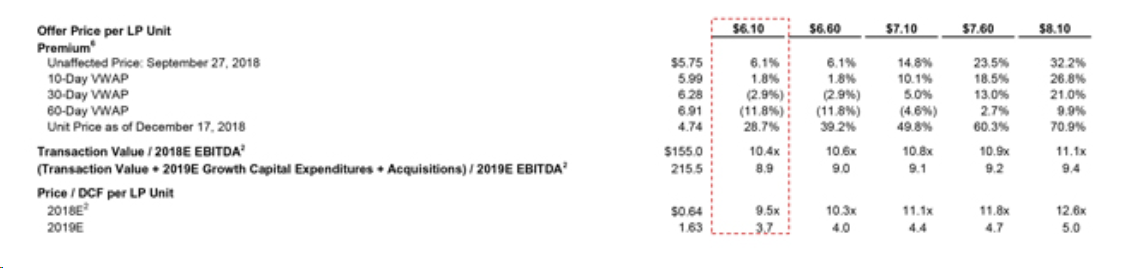

- On September 28th, 60 days after the 75% distribution cut and on the last day of the quarter, when “window dressing” led to temporary price weakness, ArcLight bid for Amid Units at $6.10.

- This was the second major event where there was no AMID conference call.

Conference calls allow analysts to ask difficult professional questions of the management. Those comments then help research analysts write the research reports that drive institutional and retail buying and provide feedback for inquisitive investors.

This combination of a large distribution cut, selective management silence and the abrupt bid by the AMID General Partner’s majority owner ArcLight, seems problematic.

MLP holders, in general and like our clients, are retired or elderly. They own MLPs for the yield to provide income for their retirement expenses. Retired and elderly investors in particular cannot afford capital losses as they have limited earning capacity to recoup capital losses. So when ArcLight bid for AMID units, it pitted the most sophisticated professional energy investors with access to inside information against retired and elderly individuals who expect management to act in the interest of unitholder and who are completely outmatched in their ability to assess corporate developments, legal implications, business conditions, business prospects and or valuation analyses compared to ArcLight, the majority holder of American Midstream Partners, GP, LLC.

The unfortunate consequence of this situation is that elderly shareholders have been shaken out of their position or are being forced to accept a loss or a bad unit price before enough time had elapsed to reconstitute the shareholder base with new investors in AMID or see the benefits of the restructuring strategy implemented, before Arclight bid 50 cents on the dollar for their retirement assets. Further, the ArcLight bid added another element of confusion which, due to the absence of normal conference calls, was not addressed.

Strangely, Lynn Bourdon did not reject the bid outright. Normally, when a company is bid for, the CEO routinely rejects the bid as “inadequate”. Nor did Bourdon request a stand still period, so that the benefits of the new strategy could accrue to the unit holders. Nor was there any apparent effort made to hold an auction for the AMID assets following ArcLight’s bid. Why not bring in a comparably sophisticated buyer like Energy Capital Partners, Riverstone Holdings or Enterprise Product Partners, LP (EPD)? No such unitholder friendly actions were made despite Bourdon’s effusive recommendation to buy AMID Units in the $13 range 10 months prior.

{kind=link}

- Bloomberg reporter Rachel Heard Adams reported that Recurrent Advisors’s Co-Founders Brad Olsen and Mark Laskin had sought to stop the deal, challenging both the governance and bid price offered by ArcLight. Olsen, a former UBS MLP investment banker compiled a study of all GP LP bids, which showed that every preceding GP LP transaction occurred within 30% of the MLPs’ highs. ArcLight $ 6.10 bid was priced within 30% of its all time low price. His comprehensive report mailed to the independent directors on October 4th 2018 suggested that AMID was worth $15-20/unit.

Having read both the Evercore research and that of Recurrent Advisors valuation study, it is hard not to see Recurrent Advisor’s work as the more credible and objective of the two. Further, we have been informed that Evercore is a repeat investment banking client of ArcLight, which would lead one to believe that their selection of Evercore might have been was conflicted and improper.

As we have previously written, the distribution cut of July 27th did not change AMID’s cash flows or asset values. In fact, the distribution cut was to accelerate the deleveraging and the swapping of non-core assets with identified accretive assets. We also wrote to the board asking for a delay or an auction so that the market pricing mechanism could work effectively. Their response can be read here.

- The fourth quarter was a tough one for the energy and equity markets.

- On December 31, four days after the decision and through an SEC filing—with no press release nor conference call–AMID wrote that due to a convoluted renegotiation of a covenant, AMID would not pay its fourth quarter distribution. Further, AMID would not reinstate its distribution until its EV to EBITDA ratio was below 5.0. With little analyst coverage, on New Year’s Eve, on the day when tax loss selling and window dressing are the greatest, this distribution bombshell created a selling panic and AMID LP units dropped 39%. AMID traded to $2.75/unit on 9 times normal volume.

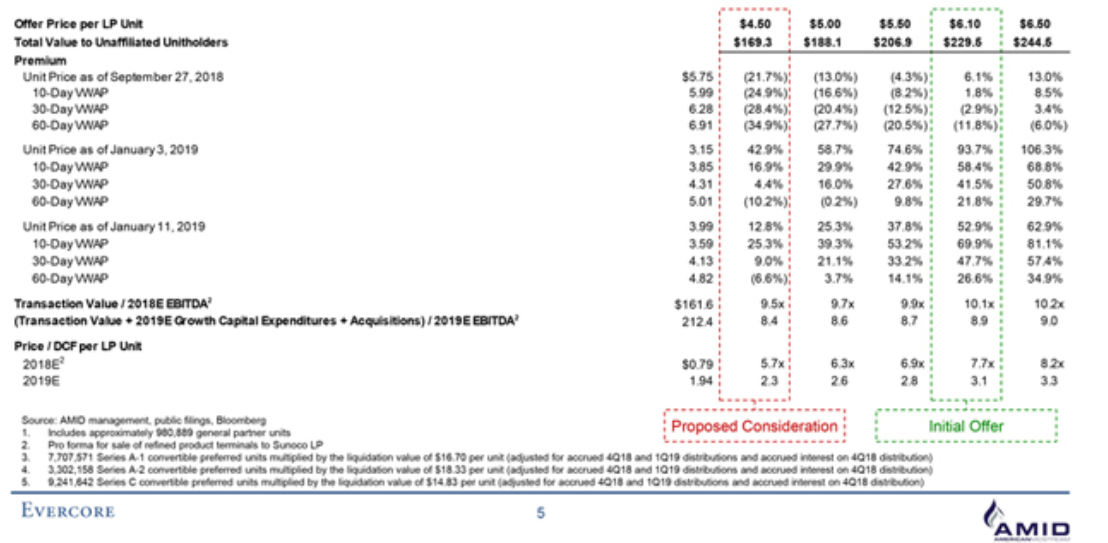

- Then, on January 3rd, ArcLight bid $4.5, below its previous $6.10 bid arguing that conditions had worsened and a lower bid was in order. This representation of operating conditions by ArcLight to the Independent Board Members(Mr. Peter A. Fassulo, Mr. Donald R. Kendall Jr., and Mr. Gerald A. Tywoniuk), was inaccurate because on January 11th, 2019, LLOG, the independent operator of Delta House, announced that Delta House was operating at maximum capacity.

AMID Unitholders reasonably expected, based on the stated objective of the distribution cut and capital allocation strategy, that management would time allow for the benefits of the new capital allocation strategy be implemented.

- Since the beneficiary of the transaction is ArcLight and the losers are AMID Unit holders, it was(is) up to conflicts committee (Mr. Peter A. Fassulo, Mr. Donald R. Kendall Jr., and Mr. Gerald A. Tywoniuk) to act in a manner that is clear, transparent, fair and impartial. Evercore was retained by the conflicts committee.

- January 10th, Save Unitholders’ Craig Thomas press released the following article recommending unit holders contact the conflict committee, writing the units were worth at least $9/unit. https://www.globenewswire.com/news-release/2019/01/10/1686063/0/en/Concerned-Unitholder-Encourages-AMID-s-Three-Independent-Directors-to-Reject-Publicly-Sponsor-s-Take-Private-Bid-and-Immediately-Implement-Other-Steps.html

Numerous opportunities for discussion or financial disclosure not made available.

- When the fourth quarter K-1 was to be released, AMID announce that it had agreed to be sold for $5.25, and that there would be no shareholder vote or meeting. “As a result of the pending merger, the Partnership will not hold a conference call in connection with the issuance of this earnings release.”

- On May 20, 2019, AMID announced that it was asking bond holders to accept a consent solicitation whereby updated operating data does not have to be provided to the SEC. American Midstream Announces Consent Solicitation with respect to 8.500% Senior Notes due 2021

When the first quarter’s earnings came out, the earnings were strong.

- On May 10, AMID released first quarter earnings without a conference call. “Adjusted EBITDA (1) was $54.7 million for the three months ended March 31, 2019, compared to $52.4 million for 2018. Total segment gross margin (1) was $71.2 million for the three months ended March 31, 2019, compared to $64.7 million for 2018.”

The Adjusted EBITDA for the first quarter 2019 exceeded all of 2018 quarters’. Adjusted EBITDA is the preferred non-GAAP metric. These numbers are consistent with the valuation levels argued by Bradley Olsen, what we estimated and what Craig W. Thomas argued in January and forecasted. These earnings numbers suggest that $5.25 is woefully below fair value.

- We calculate that based on the latest earnings, the latest annual Distributable Cash Flow is about $100mm annually. At a 10 multiple and 54.5 mm shares, the units are worth $18.5.

In our opinion, the valuation work by Evercore has significant fundamental flaws. These studies were released through the SEC Edgar database on April 24, 2019. EDGAR Filing Documents for 0001193125-19-117158

Our primary issues are the use of stub valuation metric for the step down in volumes at Delta House and the overuse of VWAP methodology.

- The introduction of a stub

valuation to treat the step down in Delta House, raises two questions.

- Was the stub valuation method used by Evercore now that ArcLight is the buyer, also used when these Delta House assets were dropped down to AMID (sold)?

- Given the complexity of the valuation exercise, why didn’t the management or conflict committee seek to solicit outside bids in order to find fair value?

- VWAP is a trading metric which calculates the Volume Weight Average Price of an institutional stock trade. Using VWAP is logically flawed when used in the immediate aftermath of a distribution cut like after the July 26th 75% distribution cut or the December 31, distribution elimination when market is in disarray and not representative fair value.

MLPs are income securities. They are not actively traded large capitalization securities where a VWAP analysis might be more appropriate. Due to the significant change in the distribution policy, there had been a dramatic volume spike in selling caused by income investor reflexively selling. It consequently takes time for the shareholder base to be reconstituted (new income investors would have to buy AMID units to replace those who left and reverse the trading imbalance.) This takes several months or even a year, especially when there was an absence of management Q&A, limited conference calls and when AMID is a relatively unknown illiquid security.

In the data box below, Evercore benchmarks the bid price against the 10 day VWAP, the 30 day VWAP and the 60 day VWAP. Due to the market impact of a distribution cut, no market measure should be used as a valuation metric. Its inclusion defies the logic of a serious valuation exercise, so critical to the concept of a “Fairness Opinion.”

https://www.sec.gov/Archives/edgar/data/1513965/000119312519117158/d733891dex99c3.htm

{kind=link}

https://www.sec.gov/Archives/edgar/data/1513965/000119312519117158/d733891dex99c4.htm

The validity of a VWAP in the aftermath of a distribution cut is flawed even when repeated. In the databox below, the misapplication of VWAP as a legitimate valuation tool is repeated three times. First related to the September 27th bid, following the 75% distribution cut of July 26th. The second and third use are even more illegitimate in that they are measured from literally within one and three weeks after the distribution elimination.

{kind=link}

Our analysis is neither detailed nor exhaustive. Consider that ArcLight held debt, which could have been extended, avoiding a going concern note, is one of the areas we have not covered. If the sponsor were seriously “supportive”, why was ArcLight allowing a “going concern” note for AMID while they were actively bidding for the stock?

The flaws we have identified certainly challenge the voracity of the materials provided by Evercore. In comparison to the analyses by Recurrent Advisors and Save Partners’ Craig W. Thomas, the valuation differential is quite significant. Arguably AMID is worth 2 to 3 x the $5.25 price the conflicts committee Mr. Peter A. Fassulo, Mr. Donald R. Kendall Jr., and Mr. Gerald A. Tywoniuk approved.

- One legal concept that may be relevant here is the concept of intent. It shocks me that this transaction was entitled “Project Harpoon”, before the December 31, distribution elimination.

- Recurrent Investment Advisors co-founder Bradley Olsen said “The pattern and behavior of the second bid is obviously the same pattern and behavior of the first bid,” to Bloomberg reporter Rachel Heard Bradley Olsen…. “The initial read of the second bid is it seems to be using a set of circumstances that were created by an ArcLight board and ArcLight-appointed management team as an excuse to lower the bid.”

Varsity Blues

In light of the “Varsity Blues” college admissions rigging scandal where the rich tried to bribe their way for their children to get into top schools, this ArcLight AMID transaction stands out. “Through a generous gift from Daniel Revers T’89, managing partner and co-founder of ArcLight Capital Partners and a member of Tuck’s board of advisors, Tuck launched the new Revers Center for Energy, established to inspire and shape tomorrow’s leaders in energy while engaging in today’s energy economy.” ArcLight’s CoFounder and Managing Partner is Dan Revers. Further the head of the conflict committee is David Kendall who is also on the Board of Trustees for the Dartmouth Tuck School of Business.

If this is an unfair deal, which we think it is, does Dartmouth or any University want such operators prominently associated with their school, even though they may be significant benefactors?

This transaction is stingingly ironic. One of our clients, who has lost heavily in AMID, is a 90 year old World War II veteran. He was an auditor for an international accounting firm. He is also a Dartmouth graduate with several relatives who are Dartmouth alumni. Another client with large losses in AMID is a retired and brilliant doctor from Dartmouth Hitchcock Hospital.

Outside those associated with Dartmouth, our other clients’ sentiments echo “Phil from OKC” under my AMID April 18th seeking alpha comments. “I am long AMID and seething with anger at the apparent attempted theft of our investing capital, from both me and other retirees, who have spent our lives accumulating it with honest, and dedicated hard work, by the thieves at Arclight, with the likely assistance of the so-called independent directors. Your article is so well researched and written, I am going to be including it as an attachment to both of my Senators as well as my Congressman, to see if we can put on the brakes to the consummation of this buyout.”

Perhaps Harvard Business School, who pioneered the case study, should make a case study of this transaction. This transaction would be a great teaching moment and exercise for any business school student. The accounting is complex. There are complex legal issues, and, most importantly, issues of ESG Environmental, Social and Governance criteria. While this transaction is a fabulous case study and teaching moment, a public review might cancel this transaction as its study might lead to a decline in assets from Universities and other institutions with ESG mandates.

Buy AMID:

We believe that class action attorneys will litigate this transaction. If the court determines that a compromise fair value is $10/share, shareholders of record could find themselves with a lottery ticket. Frequently class actions result in most of the spoils accruing to the lawyers. This time is different. Even with one third of the take going to the attorneys, shareholders of record could earn $1-2/unit. With a cost basis of $5.25, a $1-2 in legal compensation, a 20-40% return could be had for an investment that unit holders who may only own AMID for a few weeks.

With an energized slew of presidential candidates waging war on the top 1%, white privilege, old boys’ networks, the prospect that this transaction might not close is not an impossible dream.

Sincerely,

Tyson Halsey, CFA