The potential financing of Driftwood LNG is a rare asymmetric opportunity that we detail in this note. However, we include yesterday’s YouTube update by Charif Souki the Executive Chairman of Tellurian Inc. His commentary confirms our understanding of the opportunity that, with this note, highlights the compelling investment financing and return details sought by serious investors.

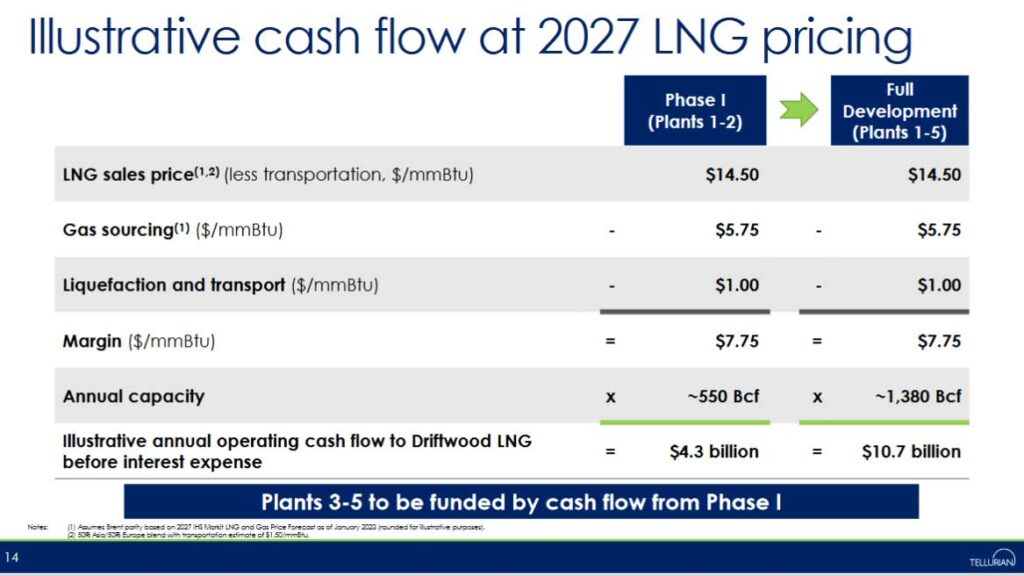

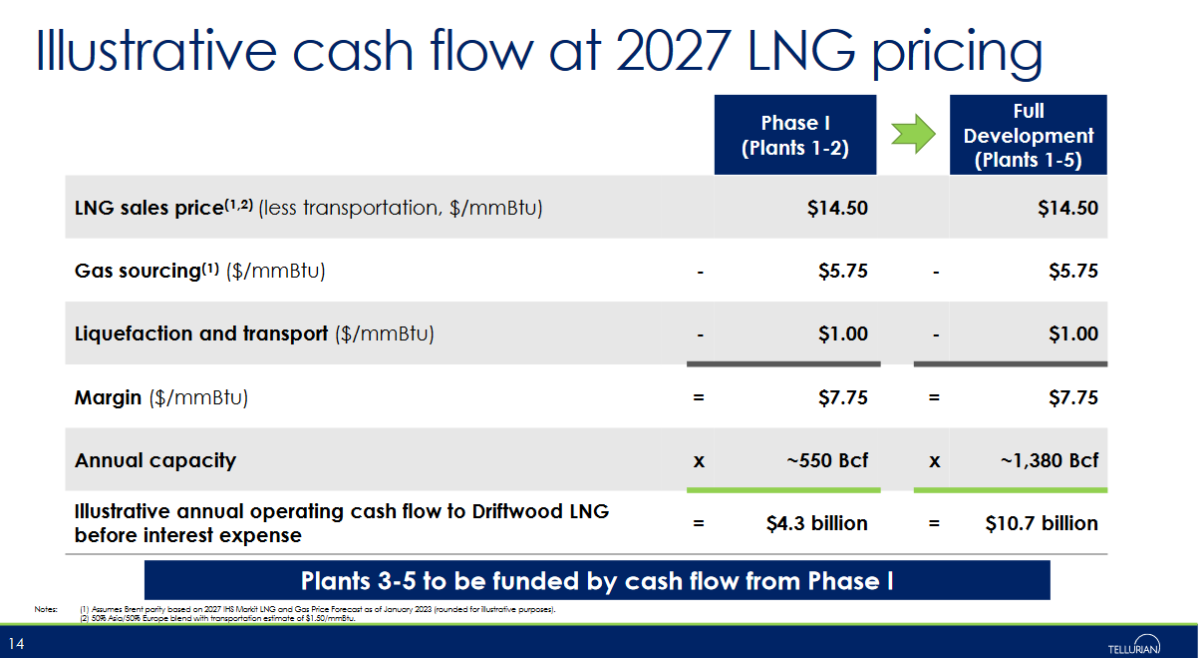

Tellurian’s return profile is different than most companies’ because its return potential is directly linked to the financing and construction of the Driftwood LNG liquefaction facility. Typically, companies are valued on their prospective operating metrics. In the case of Tellurian, the price of its shares is a function of their prospects for successfully funding Driftwood LNG which should generate about $10.7 billion in cash flow in 2029.

Tellurian’s stock price is $1.36/share COB April 21, 2023. The company has 564,000,000 shares outstanding and a market cap of $766,000,000. If Tellurian’s 2029 cash flow projection of $10.7 billion proves accurate, then at five times cash flow, the company’s future market capitalization could be $53.5 billion. If the company has one billion shares outstanding in 2029, then a stock price target on the order of $53/share is a reasonable estimate.

The 2029 $10.7 billion cash flow illustration shown below comes from Tellurian’s February Investor Presentation. Whether that cash flow is achieved is entirely dependent on whether Tellurian can secure the funding to build Plants 1 through 5 of the Driftwood LNG liquefaction plant. When sufficient funding is secured a “Full Notice To Proceed” FNTP will be issued by Bechtel, the world leader in liquefaction plant construction, to complete Phase One: Plants 1 and 2 of the Driftwood LNG project. Plants 3, 4 and 5 will be funded with cash flows from Phase One.

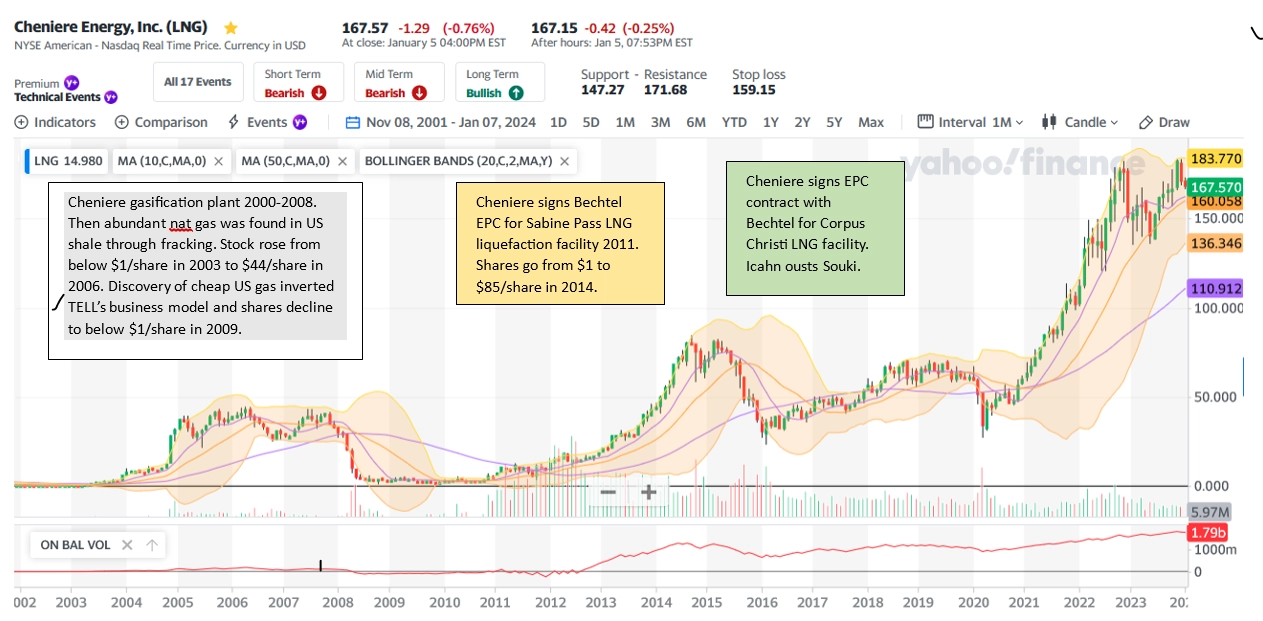

To understand Tellurian and Charif Souki we looked at the price history of Cheniere Energy Inc., where Souki was the former co-founder and Co-CEO. In the chart below we see abnormally high rates of appreciation occurred during Cheniere’s financing and construction phases:

We have concluded that by analyzing Tellurian news regarding Driftwood’s project financing, we can potentially capture the extraordinary share price appreciation associated with the derisking periods correlated with Cheniere’s historic moves. Derisking is a step-function similar to an FDA approval for a one product biotechnology company. Traditional equity valuation methodologies such as discounted cash flows and sum of parts methodologies improperly capture the derisking import of securing the financing to announce Full Notice To Proceed “FNTP” with Bechtel. FNTP commits Bechtel to complete the construction of the Driftwood facility which effectively assures Driftwood’s delivery of LNG and future cash flows. We expect FNTP will be achieved this year based on company statements and this video update on April 5th of the Driftwood Project with construction head, EVP and President Driftwood Assets Samik Mukerjee and Executive Chairman Charif Souki. Now, with the LOI sale leaseback prerequisites due by July 14, 2023, we believe a FNTP could be announced as soon as August, and then the shares could trade at $7.5/share or about five times Tellurian’s current stock price.

A Brief History of Tellurian’s Recent Volatility:

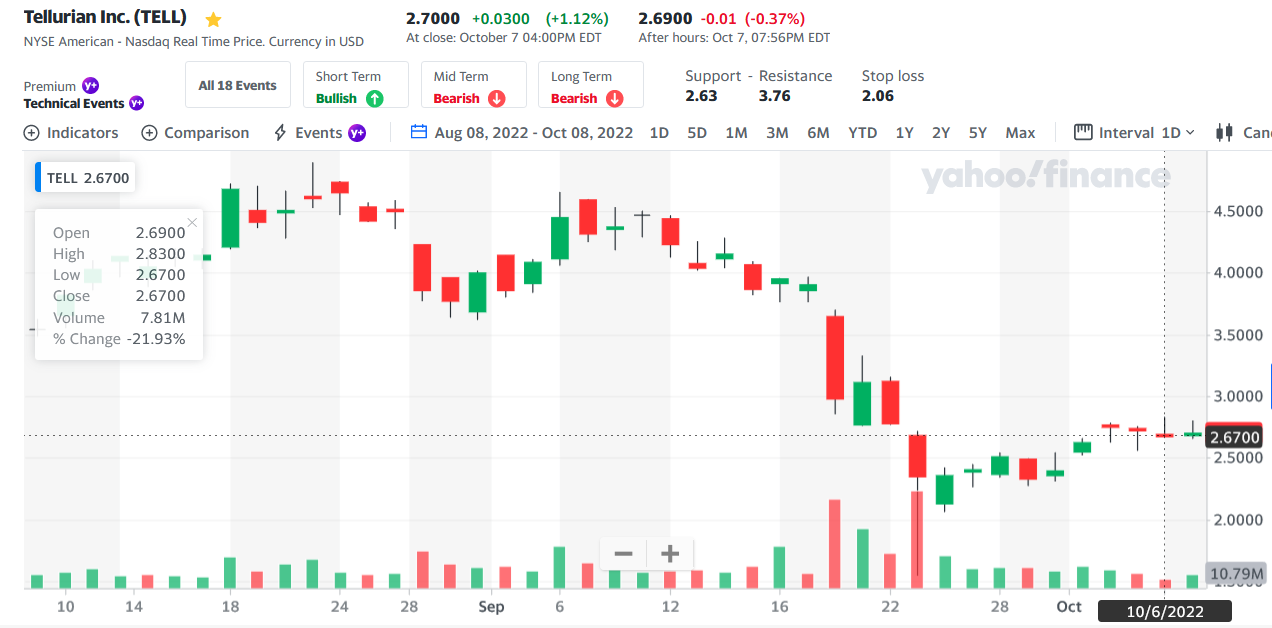

The 15 month chart below shows Tellurian’s shares rose 174%, in early 2022, when natural gas and LNG prices spiked when Russia invaded Ukraine. After May 2022 natural gas and LNG prices declined to more normal levels with prices as of April 20th, 2023 being $2.19/mmbtu for Henry Hub and $13.04/mmbtu for Europe’s TTF LNG benchmark. However, the greatest downside driver during the 76% decline from April to September came from Tellurian’s decision to cancel its $1 billion bond and warrant offering on September 19, 2022. This offering cancellation suggested a project delay and prompted the cancellation of the Shell and Vitol SPAs — though if the Driftwood LNG project look to get funded, both entities could return if new strategic investors do not displace their service offerings.

In the third quarter of 2022, Tellurian shares struggled as its financing prospects were unclear and tax loss selling weighed on the stock. In the first quarter of 2023, shares continued to be pressured due to the resignation of two board members on February 2, 2023. Furthermore, the announcement on February 13th that Charif Souki’s shares were being sold under a forced liquidation by Wilmington Trust Company associated with a substantial real estate purchase in Aspen, created horrific optics for the company. The sale of shares of the company’s public face and Executive Chairman presented the mistaken impression that these sales were a deliberate decision to exit his Tellurian investment. However, the sales were executed by Wilmington Trust and related to Souki’s real estate purchase near Aspen, Colorado and driven by the terms of the real estate loan. We suspect the potential conflict of interest of the loan terms which caused the share sales by Wilmington Trust may have been a factor in the “personal decision” by board members Claire Harvey and James Bennett to resign. These events have no material impact, in our opinion, but led to extremely negative sentiment surrounding Tellurian’s prospects, just as green shoots of a successful financing began to materialize.

Green Shoots — Credible Financing News:

During the first quarter, the board and CFO resignations, Souki’s share sales and negative momentum culminated in an extreme oversold low share price of $0.98/share on March 23rd. However, despite this horrible sequence of negative news, certain positive developments affirmed viability and the potential for Driftwood funding to be realized this year.

Here are several credible news items that support a turnaround:

- Gunvor extended its SPA on January 27, 2023. We felt if Driftwood funding was not possible, why would Gunvor extend its SPA with Tellurian?

- GAIL announced an EOI on February 17th. Since the September debt offering cancellation, Tellurian emphasized its new financing model which would utilize strategic partners and the company has publicly courted India as a logical offtaker. Consummation of this contract could lead to a significant equity investment, up to 26%, of Tellurian. The EOI “Expression Of Interest” has GAIL effectively creating an syndicate of Indian gas companies that want to secure low cost LNG for the long term.

- On February 22, 2023, Tellurian Inc. reported solid earnings. TELL demonstrated they had the balance sheet and cash flow to continue building the Driftwood foundation and targeting LNG in late 2026.

- On March 31, the company paid off its $169,165,990 in current convertible notes, sending another signal that Tellurian had the balance sheet and income to continue funding Driftwood foundational work that shortens the timeline to LNG production.

- On April 4th, a binding Letter of Intent “LOI” was signed for a sale lease back of the Driftwood property where it will receive $1 billion based upon other funder conditions being met. Since Cheniere Energy Inc., employed a MLP structure — Cheniere Energy Partners, L.P. (CPQ), selling the facility asset was a clever innovation, but not unusual.

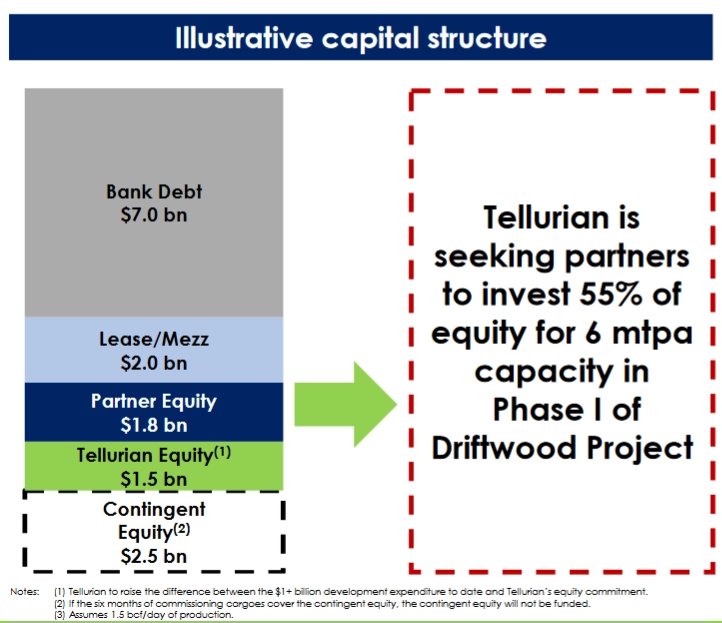

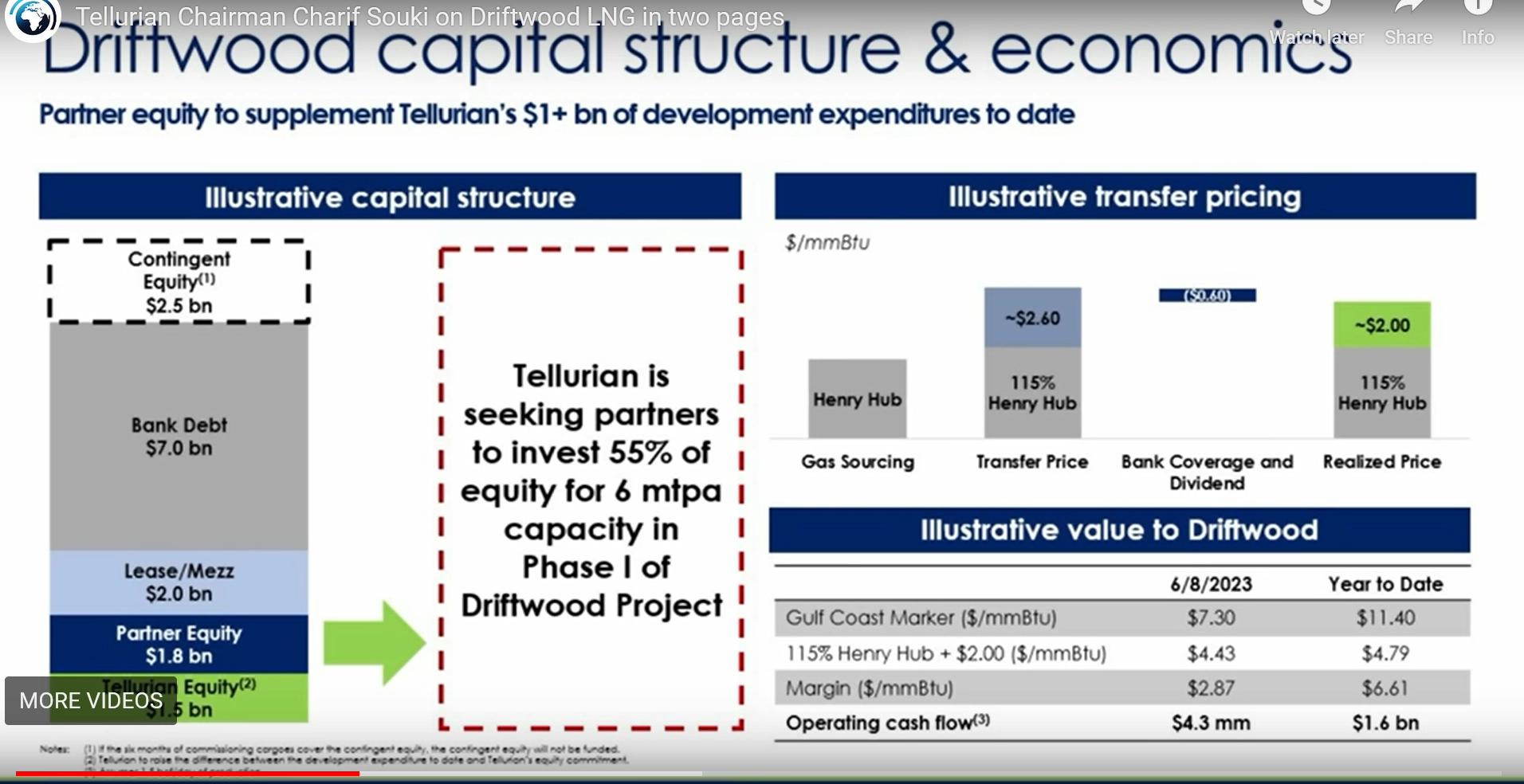

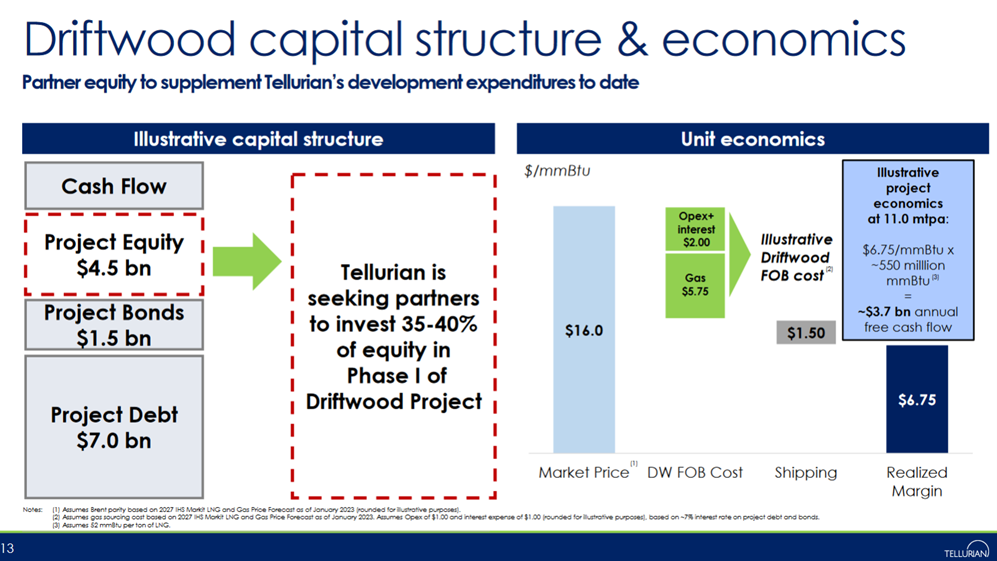

- On April 10th, Charif Souki said that all the debt, mezzanine and equity investment must close simultaneously and that “next week” Tellurian would be going to NY to secure its $7 billion bond commitment. In total, $1 billion has been invested by Tellurian, $1 billion will come from the sale lease back, and Tellurian is in the process of securing $7 billion in project debt finance. Add in a couple of strategic equity commitments and the funding levels for FNTP could be met. Also encouraging, this debt to equity ratio was just implemented in the Sempra ConocoPhilips Port Arthur LNG facility on March 20, 2023 for a similar sized project.

- The company, through its many videos and presentations, identifies a pathway to funding Driftwood. With the sale leaseback, other equity counterparties serving as contingent guarantors “of BBB credit quality” are required by July 14th to meet their pro rata obligation of the Master Lease agreement otherwise Tellurian will not secure its $1 billion from its LOI. The final closing is 91 days later, but the syndicate for the $13.6 billion should be largely complete as of July 14, in our opinion. $6 billion in equity and mezzanine finance and $7 billion in project bond finance is the current capital structure. This is juxtaposed to the “Topco” level $1 billion bond offering 11.25% with warrants in September. The current structure utilizes “project bonds” that are an obligation of the Driftwood project. Banks view projects with known feedstock providers, off takers, a proven process technology and contracts, are considered high quality (lower cost) “project finance” debt. Tellurian’s Investor Presentation suggests a 7% interest rate. We believe that a FNTP could be secured in August before the final closing of the sale lease back contract in the third quarter of 2023. This capital structure is lower risk than what Tellurian had been targeting in August and September 2022, due to a higher equity component and lower debt ratio.

- April 20, 2023, FERC announced the 200/300 pipeline approval Driftwood Pipeline, LLC. This pipeline permission connects existing pipelines with access to the Haynesville shale to the Driftwood LNG facility. This should eliminate any concern from Haynesville E&Ps, who could be strategic equity funding partners, that they might be hindered in delivering their natural gas to the Driftwood LNG facility.

We see green shoots and funding coalescing for Driftwood, catalyzed by the $1 billion sale leaseback financing structure announced on April 4th, 2023. This funding should close 91 days after the guarantor affirmation date of July 14th or July 31st. Consequently, we assume that by July 14, the $7 billion in project debt finance and the $1 billion sale lease should be affirmed, which, in combination with some strategic equity investors, could raise enough capital to secure the FNTP from Bechtel in the third quarter. With Driftwood’s completion prospects being assured by the FNTP, we could see the stock price rising to $7.5 by August 2023 if not later in the third quarter.

Risk and Return Evaluation:

Downside Risk:

There are many market risks especially in terms of natural gas and LNG market price and market demand. Furthermore, there is a strong anti-fossil fuel lobby which works to stymie the global adoption of LNG. These anti-natural gas forces are countered by empirical evidence that highlights natural gas and LNG benefits including increasing energy security, reducing carbon emissions by replacing coal fire electric plants with natural gas, and ending poverty and hunger through broader adoption of US natural gas and LNG in harmony with the increased deployment of renewable energy, hydrogen, and nuclear.

The downside risk to Tellurian is its liquidation value. Assuming the value of Driftwood LNG at its current state is $0, then the company’s current value is only the value of its natural gas pipelines which should generate about $150 million in EDITDA at today’s low gas prices, plus its properties and pipelines. This should be worth about $500,000,000.

Even if Tellurian cannot finance Driftwood, there may be larger entities that would buy the Driftwood LNG Property and licenses for $500,000,000. Consequently, we estimate that the downside risk and downside price valuation for Tellurian based on a market capitalization of $500,000,000 without Driftwood and $1,000,000,000 with an unfunded Driftwood. We estimate the downside risk is $0.88/share to $1.76/share, if we divide these two market capitalizations by the current share count of 564,000,000.

Valuation:

These calculations should be considered as an order of magnitude study. The key is how significant the derisking element is to the price appreciation. We think FNTP, Phase 1 completion and Phase 2 as three derisking milestones.

We estimate that in 2029, Phase 2 will be complete and the market valuation for Tellurian will be five times the illustrated $10.6 billion in EBITDA or $53 billion. Assuming dilution we estimate one billion shares outstanding in 2029, and a share price for TELL of $53.

This would imply an annualized return over 6 years of $53/1.36^1/6-1=83% annualized.

If expected funding steps are completed on schedule, we estimate Tellurian to achieve FNTP in August and then the stock would trade at $7.5/share.

We also estimate TELL’s further rate of appreciation if TELL shares rise to $7.5/share in August when Driftwood should get its FNTP from Bechtel. Based on those assumptions, we estimate the return from our August $7.5 price target to be $53/7.5^1/(5.6)-1 = 41% annualized from FNTP to 2029.

We think the critical derisking point will be when Driftwood starts producing LNG and generating cash flow with the completion of Phase One (trains/Plants 1 and 2) in late 2026 or early 2027. Consequently, at that point the shares could be a good bit higher. We estimate a $34.8/share price target for the completion of Phase 1 based on a 15% annualized discount to the 2029 $53/share price target we envision.

Conclusion:

Tellurian appears to be moving toward successfully financing its Driftwood LNG liquefaction plant in Lake Charles, Louisiana. LNG capacity is experiencing a second wave of project development to address the supply gap in liquefaction capacity as a result of Russia’s invasion of the Ukraine. Furthermore, energy policy is moving from eliminating all fossil fuels in favor of renewables to one that includes transition fuels like natural gas and nuclear energy. Both natural gas and LNG can help end poverty and hunger globally more rapidly than a renewables only strategy.

Tellurian’s management team has a world class record. Its Principals Charif Souki, Octavio Simoes and Martin Houston have collectively built about 80% of US liquefaction facilities and 60% of global LNG facilities. The Driftwood facility is fully permitted, and FERC approved. Tellurian’s prospects now lie in its ability to finance Driftwood.

This sale leaseback will provide Tellurian/Driftwood with $1 billion in cash.

I believe next steps will be a Heads Of Agreement with GAIL based on the EOI. GAIL could provide up to $3.5 billion, but US Nat Gas E&Ps and IOCs like Shell, BP, and Saudi Aramco could all kick in equity. GAIL would provide an end market buyer of LNG demand which will derisk the project and inspire the equity investors.

Then with this binding sale leaseback LOI, TELL should be able to fund its mezzanine $1.5 billion piece. I believe that will be funded by infrastructure or PE investors. The remaining $3-3.5 billion will come from strategic investors like GAIL, US nat gas E&Ps, and or International Oil Companies like Shell, BP, Saudi Aramco…. I believe strategics will want to negotiate transfer or liquefaction fees and terms which are more operator specific than just a financial instrument which is what the mezzanine piece is.

Yesterday’s site visit with Samik Mukherjee emphasized that Driftwood is targeting the FNTP which is the affirmation and commitment of Bechtel to complete the whole project. I believe this is the critical derisking inflection point.

FNTP will not require all $14 billion. Rather a $6 billion equity commitment plus (estimate) $3 billion in project finance debt.

This will allow Driftwood to fund all the compression and liquefaction equipment and construction and debt expenses until they raise the last debt pieces later in the year or 2024, 2025, and 2026.

Timeline:

Heads of Terms with GAIL April-May

Mezzanine Piece: $1.5bn April-May

Remaining Strategic Equity investors: 4.5bn (one billion already contributed to Driftwood from Tellurian investments to date. I believe this could be a larger amount and that would make the debt side less burdensome. May-June

Sale leaseback contingent equity partner approval should happen by July 14, 2023. Closing 91 days after July 31 when sale least back must close. June-July

Sufficient debt will be raised between July 31 and October 31 to secure FNTP and assure the closing of the funding needed for Phase One. July-October

SPAs may then be brought in depending on Driftwoods needs. Shell who had been an SPA holder could be equity provide and provide SPA services. July-October

As each of these milestones is achieved, the project is derisked. Up until today the future Driftwood cash flows were aggressively discounted and valued at the $100million or less value. As the discount rates reduce and prospects for funding increase incrementally through each milestone, the value of Driftwood should rise sharply.

For this reason, we see the stock starting to move rapidly higher to $10/share by year end.

Charif Souki, the Executive Chairman of Tellurian (TELL) was the cofounder and co-CEO of Cheniere Energy (LNG). Cheniere rose from $1 per share to $175/share between 2010 and 2022. Souki was pushed out of Cheniere, in a boardroom fight instigated by activist investor Carl Icahn. Despite Icahn seizing control of Cheniere, it was Souki who was the LNG pioneer that built Cheniere. In our opinion, TELL could be as lucrative as Cheniere for investors.

A close evaluation of Cheniere’s explosive moves (10/2002 $0.48/share to 4/2006 $43.72 and 9/10 $2.50/share to 9/14 $80.03/share) shows that these moves, 269% annualized and 138% annualized, occurred during the finance and construction stages of Cheniere’s two facilities. The first facility was a gasification facility which took cheap international sourced LNG and gasified that LNG to produce cheap natural gas for the US market. When the fracking boom took off in the early 2000s enabled by hydraulic fracturing and horizontal drilling, massive low cost natural gas was discovered in the US. This business plan reversal forced Souki to scrap his first facility and build Cheniere’s LNG facility at Sabine Pass, transforming Cheniere Energy, Inc (LNG) into the largest LNG exporter in the United States.

Today, Tellurian is poised to finance and construct its liquefaction facility, Driftwood LNG, in Louisiana. If our calculations and hopes prove to be correct, Tellurian should achieve Full Notice To Proceed “FNTP” with Bechtel, or final investment decision “FID” on the $14 billion Driftwood facility by year end. With FID or FNTP, Driftwood’s project financing would be assured and the construction of the facility would be the final step for Tellurian to complete before Driftwood generates cash flow. Based on the explosive returns that occurred during the financing and construction periods for Cheniere Energy, in the chart illustration above, we believe that Tellurian stock could trade at $10/share by year end when financing is fully secured. Additionally, Tellurian’s public shareholders should be able to generate $9 billion in cash flow in 2029. Depending on international LNG prices in 2029 and afterwards, Tellurian could trade around $42.8/share based on a $7.5mmbtu spread and one billion shares outstanding. From $1.21/ share, that is about a 35 bagger as Peter Lynch would describe his greatest performing growth stocks.

LNG and Natural Gas are Transition Fuels:

UN Global Sustainable Development Goals, COP Conference of the Parties to the United Nations Framework Convention on Climate Change, and the popular fight against climate change are significant movements that have gained tremendous momentum in recent years. Two of the popular goals is the elimination of all fossil fuels and net zero carbon by 2050. These goals are proving impossible and made undeniably clear by the Russian invasion of Ukraine and it’s exacerbating the energy crisis. The rapid and unilateral transition from fossil fuels to renewables is impossible. While efforts to reduce greenhouse gases will not abate, it is increasingly becoming clear that the world will need to utilize fossil fuels through 2050. This is especially true if UNSDG Goals 1 and 2, No Poverty and Zero Hunger, are seriously addressed.

To generate enough energy to power economic growth with the least amount of carbon emissions, natural gas is a far superior energy source to coal and oil.

The environmental benefit of swapping coal with natural gas to generate electricity has been estimated to be so beneficial to the environment that it would exceed the environmental benefit of converting traditional automobiles to electric vehicles. EQT Inc., the largest natural gas producer in the country, provides a detailed analysis of the environmental benefits of coal to natural gas conversion. The company maintains that “replacing international coal consumption with LNG is the largest green initiative on earth.” Further,

“by 2030, emissions reductions of US LNG of international coal can be the equivalent to all three of these combined:

- Electrifying 100% of US cars.

- Rooftop solar on every US home.

- Doubling US Wind Capacity.” Source: EQT PowerPoint

EQT is looking to invest in LNG facilities so it can convert its natural gas into LNG and sell its cheap US natural gas at high international gas prices.

It is particularly encouraging to see that India, the fourth largest economy in the world, is focused on converting its coal fired electric power plants to natural gas. Tellurian has indicated that India is a logical LNG (Driftwood) partner as the country seeks to reduce its pollution and grow its economy.

LNG Market Forecast:

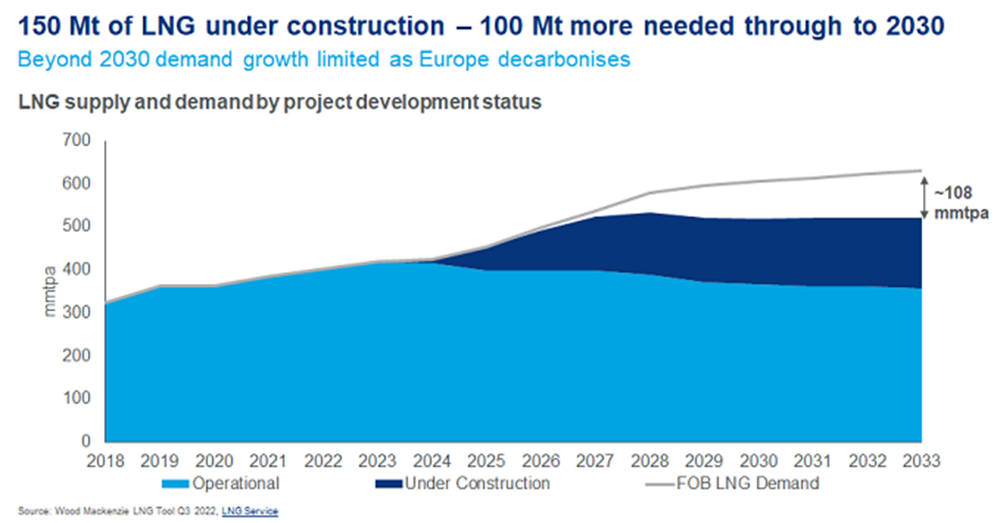

Wood Mackenzie estimates an additional 108 MTPA of LNG is needed through 2030. The chart below shows the needed additional 108 MTPA gap between existing projects, projects under construction, and planned projects — where Driftwood fits.

This video shows Tellurian CEO Octavio Simoes suggesting that Tellurian is working with India’s Energy Minister Hardeep Puri on developing such an off take agreement to help India with its enormous growth prospects and its challenging air pollution problem. Building on this, as reported in The Economic Times in October 2022, Indian Oil Corp was in discussions for potential Driftwood equity and offtake. These reports encourage our belief that GAIL could be a strategic investor in Driftwood.

A Short History of Tellurian’s Wild Price Swings:

Tellurian’s stock price swings hinge off financing prospects of Driftwood. Since Driftwood is Tellurian’s cash flow crown jewel, Tellurian shares’ price action is directly traceable to the market’s confidence in the funding probabilities for Driftwood. The chart below shows how funding prospects were initially high for Tellurian in 2017, however, failure to successfully finance Driftwood, under the leadership of former President and CEO Meg Gentle, led to the stock’s shares trading from $20/share to $10/share, before Tellurian shares crashed to below $1/share in 2020 during the COVID-19 stock market and oil price collapses. Charif Souki, who has a reputation as a risk taker, suffered margin calls, resulting in Tellurian stock liquidations at that time. In June 2020, Souki was named the Executive Chairman of Tellurian and took the reins of the company from then CEO and President Meg Gentle.

From April 2022, Tellurian’s stock experienced a brutal decline from $6 to below $1 in March 2023. TELL shares now appear to be in a comparable position to where the stock was in July 2020. Both in 2020 and today, Charif Souki has been in a forced liquidation situation. The optics of the Executive Chairman in a liquidation are terrible. However, this creates a great buying opportunity when the market’s normal clearing price is pressured by forced liquidations circumstances which are temporary.

Valuation:

There are two endpoints that provide quantifiable stock price objectives for Tellurian. The first is the point where Tellurian’s financing is assured with an FID or a FNTP. The other is when the company is cash flowing on all five trains in 2029.

Assuming a five-times multiple on $4.3 billion in cash flow and a 45% equity ownership by strategic partners, we derive a market cap for Driftwood in late 2026 of $11.825 billion. Discount the $11.825 billion back by 13%/year for 2026, 2025, and 2024 = 39% discount, the present value for Driftwood would be $7.21 billion in market capitalization at year end. Assuming 720 million shares outstanding, Tellurian shares would have a share price of $10/share at year end with either FNTP or FID.

Our longer term valuation target is when all five trains are constructed. We expect that Driftwood Phase One will be complete by 2027 and each additional train will be built every nine months so that in 2029 all five trains should be producing LNG. We assume that half of the earnings from Phase One will go to the strategic investors and all of Phase Two’s earnings will go to Tellurian shareholders. In other words, four of the five trains will be producing the spread which we estimate at $7.50/mmbtu in 2029.

Using Tellurian’s presentation estimate of $10.7 billion in cash flow in 2029, 4 of 5 trains or 80% of 10.7 billion = $8.56 billion. At five times cash flow, Tellurian’s market capitalization could equal $42.8 billion in 2029. Assuming a total share count of one billion shares, Tellurian could trade at $42.8/share. From $1.2/share to $42.8/share is 36 fold over 6 years or 81.4% annualized.

The Financing Prospects:

Charif Souki gives weekly talks and recently suggested that we could see some news in the coming weeks. The company said it is in talks with private equity or infrastructure players to secure a $1.5 billion mezzanine piece of high yield/equity portion of the Driftwood project. Tellurian also said that it is in discussions with IOCs who could provide $3-3.5 billion in equity. Of the $4.5 billion in equity, Tellurian has already paid for over $1 billion in costs leaving the remaining equity sought in the $3-3.5 billion range.

The equity side is $6 billion and the debt side is $7 billion. What Souki said on March 28th, 2023 is that they are trying to get commitments and have these entities hold until all of these pieces can be closed near simultaneously. We believe that a logical announcement would be the GAIL deal whereby GAIL takes 26% of the $14 Driftwood which would be $3.5 billion. Tellurian then could get $500 million pieces from the US E&Ps and or other IOCs. The GAIL EOI was for up to 26% so other equity players could also be integrated.

Since the September’s debt with warrants cancellation, financing prospects have looked discouraging. Furthermore, two board members resigned at the end of January, as well as the CFO. It could be concluded that the company was, in fact, having difficulty funding the Driftwood facility. Additionally, Charif Souki had posted 25 million shares of Tellurian stock with Wilmington Trust to purchase a Colorado ranch in 2017. Share price weakness since September led to Wilmington Trust calling its collateral and liquidating nearly all of Souki’s 25 million shares, adding to continued selling pressure. These sales are near completion and prospects for funding are improving. Friday, after the market closed, Tellurian announced it was transferring $166 million to cover a convertible bond current liability due in May. This liability was a concern cited by Bank America’s negative February report, but with $470 million in cash on its balance sheet at year end, the liability is an inconvenience and not an existential threat.

Psychology can change quickly. With 85 million shares short and material announcements possible in the coming weeks, Tellurian shares could move higher in coming weeks and months and, by year end, be at $10/share. The author is long both stock and options on Tellurian Inc.

- Tellurian’s shares are an attractive asymmetric opportunity.

- Recent debt and SPA cancellation reactions overdone.

- Strategic investors weigh climate and energy security, not just ROI.

Shares of Tellurian Inc. (TELL) declined nearly 50% since August 24 due to the cancellation of its $1 billion note offering and the subsequent cancellation of two SPAs (Sales Purchase Agreements). We believe the declines were overreactions.

- Powell’s Jackson Hole “pain speech”26.2022

- Announcement of deal29.2022

- Hot CPI data and Dow 1000 point plunge13.2022

- Cancellation of debt deal 19.2022

- Fed hike another 75 bps21.2022

- Cancellation of SPAs23.2022 Shares traded intraday to $1.53/share on 77 million in volume.

- Brightspeed debt cancellation29.2022

Driftwood Opportunity

The investment opportunity for Tellurian Inc. lies in its ability to generate $11 billion in cash flow per year from its Driftwood LNG facility in Louisiana.

Just as Executive Chairman Charif Souki is considered a leader in the US LNG space, Tellurian’s team has great experience as well. Tellurian’s team “originated and executed c. 79% of U.S. LNG capacity development and c. 36% of global LNG capacity development across four continents.” Tellurian’s model is transformative; its integrated model seeks to capture the US versus international natural gas price spread rather than operate as a toll road process provider. Tellurian has “all FERC and DOE permits secured for Driftwood LNG terminal and pipelines.”

The chart below of Cheniere stock (LNG) shows its price performance during both facilities’ financing and construction phases and, since 2020, the international LNG price run up.

Is Morgan Stanley New Investment Banker?

How to Close Driftwood:

There is a benefit with the cancellation of the Shell and Vitol’s SPAs in that strategic funders can control who their LNG is sold to. For example, a potential funder, such as a Haynesville E&P, may want to sell to their own preferred buyers of LNG, not Shell or Vitol’s customers. The market reacted to the SPA cancellations as if the cancellation of their SPAs was because Shell and Vitol believed TELL could not secure funding. Furthermore, the lack of gasification capacity in Europe and extraordinary gas price volatility due to the Russian invasion, made the SPA terms problematic for Shell and Vitol. Both Shell and Vitol could return with revised SPAs which are priced to the market and accordant to their capacity to ship. [The 77 million share volume and price plunge to $1.58 intraday price for TELL on September 23, appears unjustified if not suspicious.]

Beyond investment return, demand for LNG can be driven by environmental concerns and energy security arguments. Following the Russian natural gas debacle, countries are increasingly interested in diversifying their supply sources. Certain European countries may want US LNG due to the absence of Russian LNG. India is a country struggling with terrible air pollution and it has indicated that it wants LNG to replace its massive coal fired electric generation plants. Worse still is the adverse health impact of people cooking in huts with wood and dried dung, which would be vastly improved by natural gas cooking common in North America.

Ideal investors in the Driftwood facility are strategic investors. That is, an entity which would enjoy a material benefit from the LNG Liquefaction facility itself. This most logical strategic investors are natural gas E&Ps in the Haynesville shale who would economically benefit from partnering with Driftwood to sell domestic natural gas at elevated international prices. Both Southwest Energy and Chesapeake Energy Corporation stated clearly in their q2 earnings calls that they are interested in selling into the international markets. Southwest Energy is 150 miles north of Driftwood and its CEO, Bill Way on its August 5th quarterly call said “We are evaluating on a risk adjusted basis, potential opportunities to benefit from global pricing by leveraging our approximate reliable long-term supply capability to help enable liquefaction projects to achieve FID.” Likewise, Chesapeake President and CEO Nick Dell’Osso said on his August 3rd conference call “we think we are a preferred seller of gas into the LNG world. We’re right there on the doorstep of the facilities, we have a tremendous amount of gas, we have good connectivity to market. There’s a lot of projects that are in the works….” Chesapeake Energy and Southwest Energy are representative and logical strategic funders of Driftwood. Charif Souki explains on May 17th how advantageous it would be to an E&P to sell its natural gas at the much higher international rates.

Since Gas Tech, we have noticed increased indications of a deal with India, where the strategic buyer, India, is an off taker of LNG. Having feedstock providers and an off takers, significantly de-risks funding Driftwood LNG. India is the fourth largest importer of oil in the world and “liquefied natural gas (LNG) imports are expected to quadruple to 124 billion cubic meters (bcm)” said Minister of Petroleum and Natural Gas. Secretary Pankaj Jain.

“India has resumed talks with Tellurian LNG as the world’s fourth-largest LNG buyer wants to strike new term deals to secure supplies” according to Energy Intelligence.

“India’s Federal Oil Minister Hardeep Puri, along with the chairmen of state-owned refiners Indian Oil Corp. (IOC), Bharat Petroleum Corp. Ltd. (BPCL) and gas pipeline utility Gail India met with Tellurian Chief Executive Officer Octavio Simoes in Houston.

Another Try

“We exchanged notes on the evolving gas markets and opportunities for Indian oil marketing companies to invest in Tellurian’s project in US,” Puri, who has been in the US since Oct. 6, said in a Twitter post Tuesday.

Petronet LNG, India’s largest LNG buyer, signed an initial pact with Tellurian in September 2019 to negotiate the purchase of up to 5 million tons per year of LNG from the 27 million ton/yr Driftwood project” according to Energy Intelligence.”

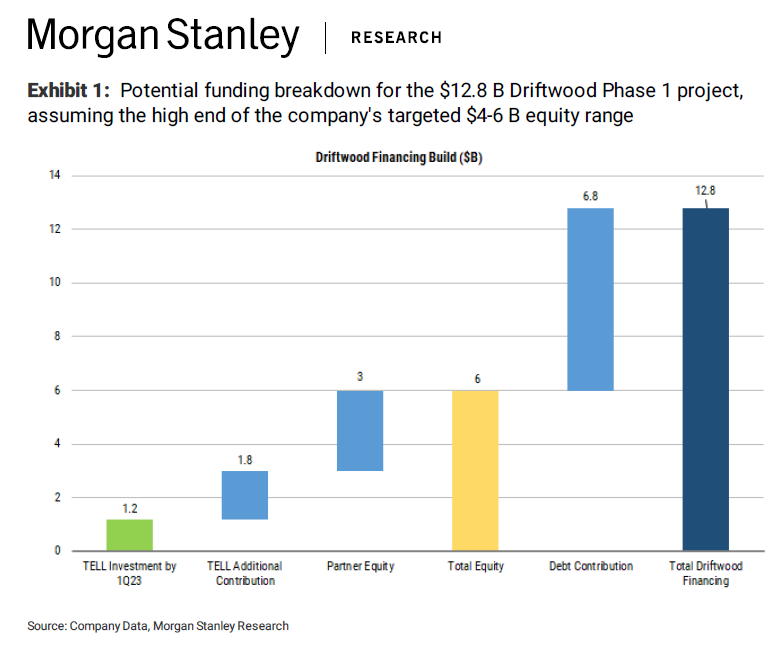

Tellurian must close this Driftwood LNG financing. We believe it will now be willing to commit up to $3 billion of its own capital up from $1 billion this summer. That $3 billion is $1.2 billion committed through q1 2023, and another $1.8 billion from future cash flows from its upstream activities from 2023-2027. The company may have targeted those additional cash flows to expand its upstream activities, but funding Driftwood is essential. Since the company, in this scenario implied by the Morgan Stanley report diagram above, is not seeking more equity capital from the $3-3.5 billion range, investors should be pleased to see the liquefaction facility get financed without meaningful additional dilution or delay. Consequently, we believe that TELL shares could exceed its spring time high of $6.2/share in the first half of 2023, and upon securing the “Full Notice To Proceed” from Bechtel, shares could top $10/share.

In recent days, stock reflects fair value for upstream and assuming cash flow will fund driftwood construction though price reflects 0% chance of success. Yesterday EQT had a positive write up. They could be in the mix with SWN and CHK.

Today, TELL put out pictures of CEO Octavio Simoes with Koreans. India and Koreans could be meaningful offtakers. Obviously Europe does not have a policy and Ukraine makes decision making tough.

Yesterday WSJ had bearish case on LNG. It is shoulder months. Cold has yet too kick in. Tax losses and recession fears are pressuring commodity prices, but I believe we are in an inflationary cycle

Check out my YOUTUBE channel.

I think there is a lot of interest and soft commitments that TELL is working to cement and that is why they say first half 2023. This is not fast enough for me, but this seems like a good prospect for a triple in 6-9 months.