- Tellurian’s Driftwood LNG project financing is imminent.

- Tellurian’s integrated model is more lucrative than tolling.

- LNG is a leading transition fuel and critical to Europe.

- Full Notice To Proceed is as important as FID.

- If successful, Tellurian could provide exceptional returns.

Company Profile and Opportunity

Tellurian Inc. (TELL) is an integrated LNG (Liquid Natural Gas) producer. TELL owns, develops, and produces its own natural gas, which comes from the nearby Haynesville Shale, which has some of the cheapest natural gas in the world. TELL is building Driftwood LNG, a liquefaction facility, which converts natural gas into LNG by freezing and compressing it 600 times. Tellurian’s forthcoming LNG production will be put on a ship FOB (Free On Board) and sold elsewhere in the world where prices are much higher. The price difference today between international LNG and US domestic natural gas (Henry Hub) is near historic highs due to poor European energy policy and the Russian invasion in the Ukraine. On August 15th, 2022, the domestic Henry Hub price was $8.73/mmBTU, the European “TTF” benchmark was $65.95/mmBTU, and the Asian Japan Korean Marker “JKM” was $45.44/mmBTU. Tellurian’s Driftwood project should generate billions in cashflow when it is built and operating in 2026.

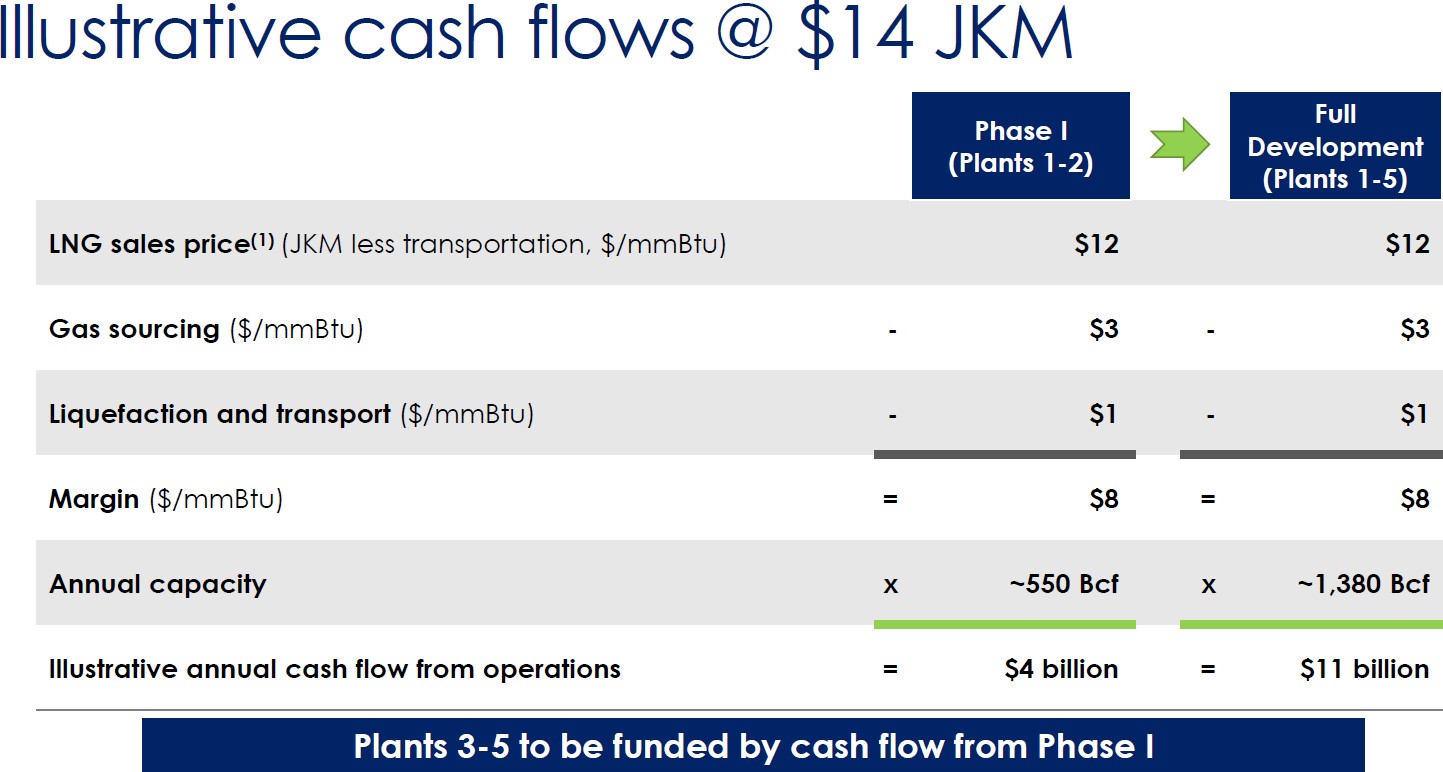

Below is an illustration, from the company’s most recent investor presentation, that shows about $4 bn in cash flow per year when Phase 1 (2 trains) is complete; and, when fully constructed with Phase 2 complete (all 5 trains), Driftwood should generate about $11bn in cash flow per year.

Source: Tellurian Investor Deck 8.2022

The project timing based on Souki’s Cheniere experience is 40-44 months from April 2022, which was when Driftwood’s construction with Bechtel commenced. This implies a completion date of September to December 2025.

Charif Souki is Tellurian’s Executive Chairman. Souki is a pioneer in the LNG industry; he was co-founder and Co-CEO of Cheniere Energy, the largest LNG export company in the US. Tellurian’s team “originated and executed c. 79% of U.S. LNG capacity development and c. 36% of global LNG capacity development across four continents.” Tellurian’s model is transformative; its integrated model seeks to capture the US to international spread rather than operate as a toll road process provider. Tellurian has “all FERC and DOE permits secured for Driftwood LNG terminal and pipelines.”

Tellurian’s high octane model requires $12.8 bn which it expects to raise through 2/3 debt and 1/3 equity. This is a difficult task, but Souki’s background as an investment banker, successful entrepreneur, and Co-Founder of Cheniere makes him a seasoned executive and successful LNG financier. As one energy banker said, “If anyone can do it, Souki can.” Not all are convinced.

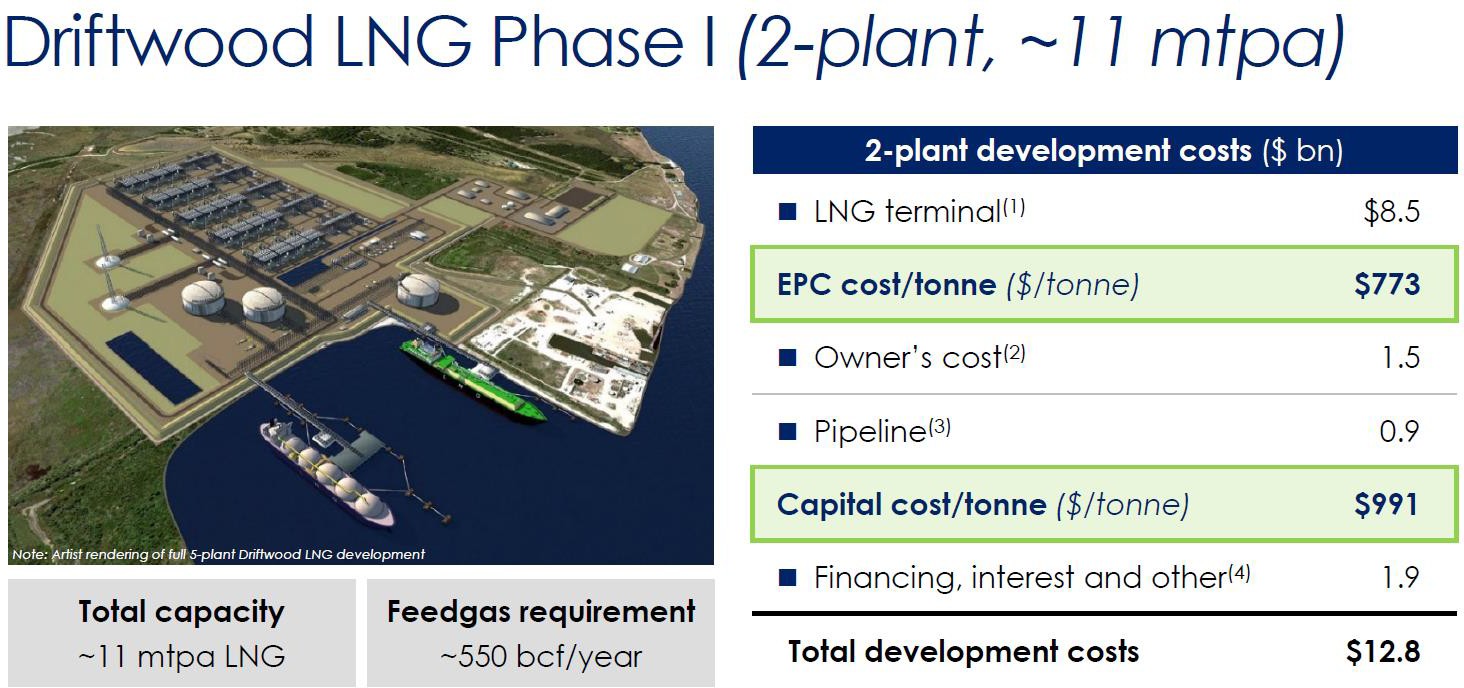

The illustration below shows the site and costs for Driftwood LNG Phase 1 facility. Once Phase 1 is completed, Tellurian looks to fund Phase 2 (trains 3,4, and 5) out of cash flow produced by Phase 1.

Source: Tellurian Investor Deck 8.2022

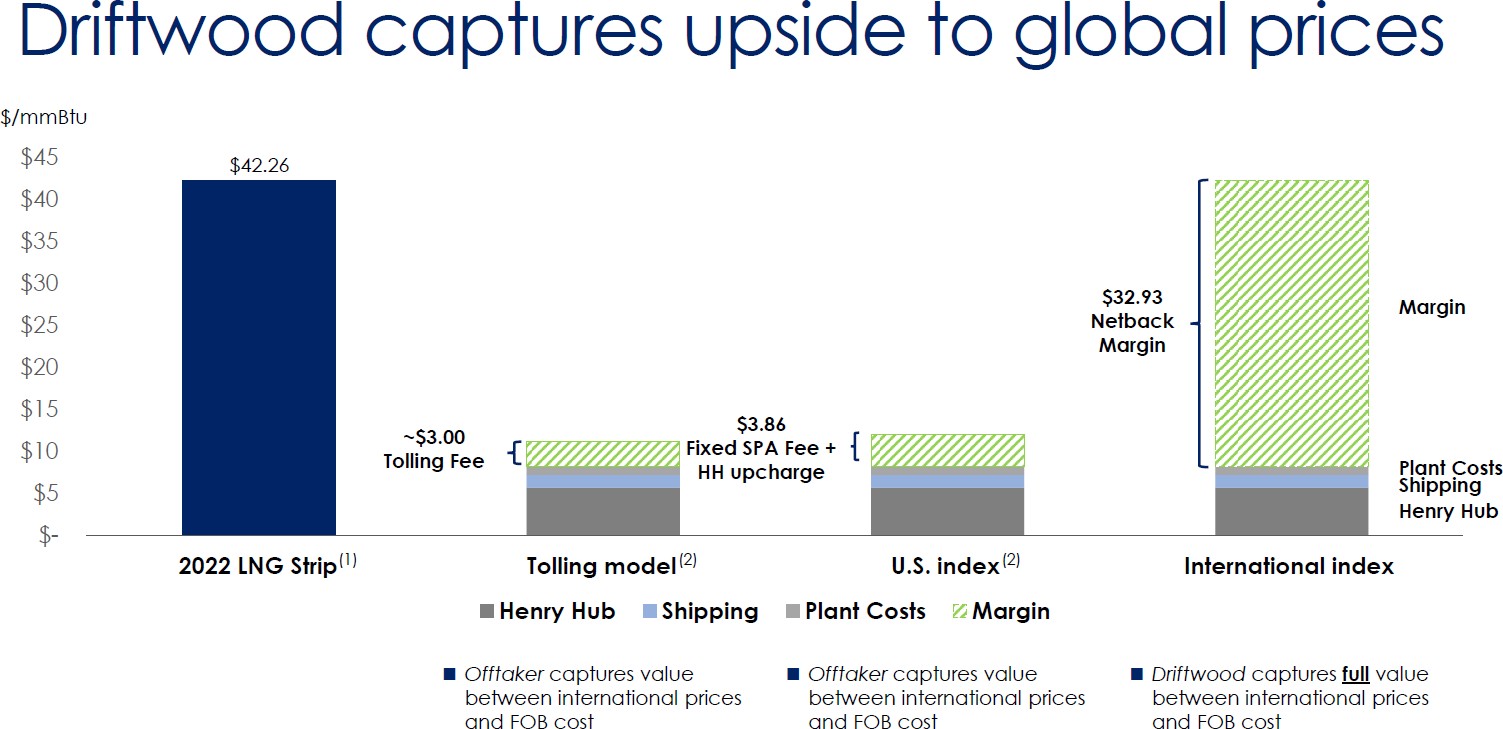

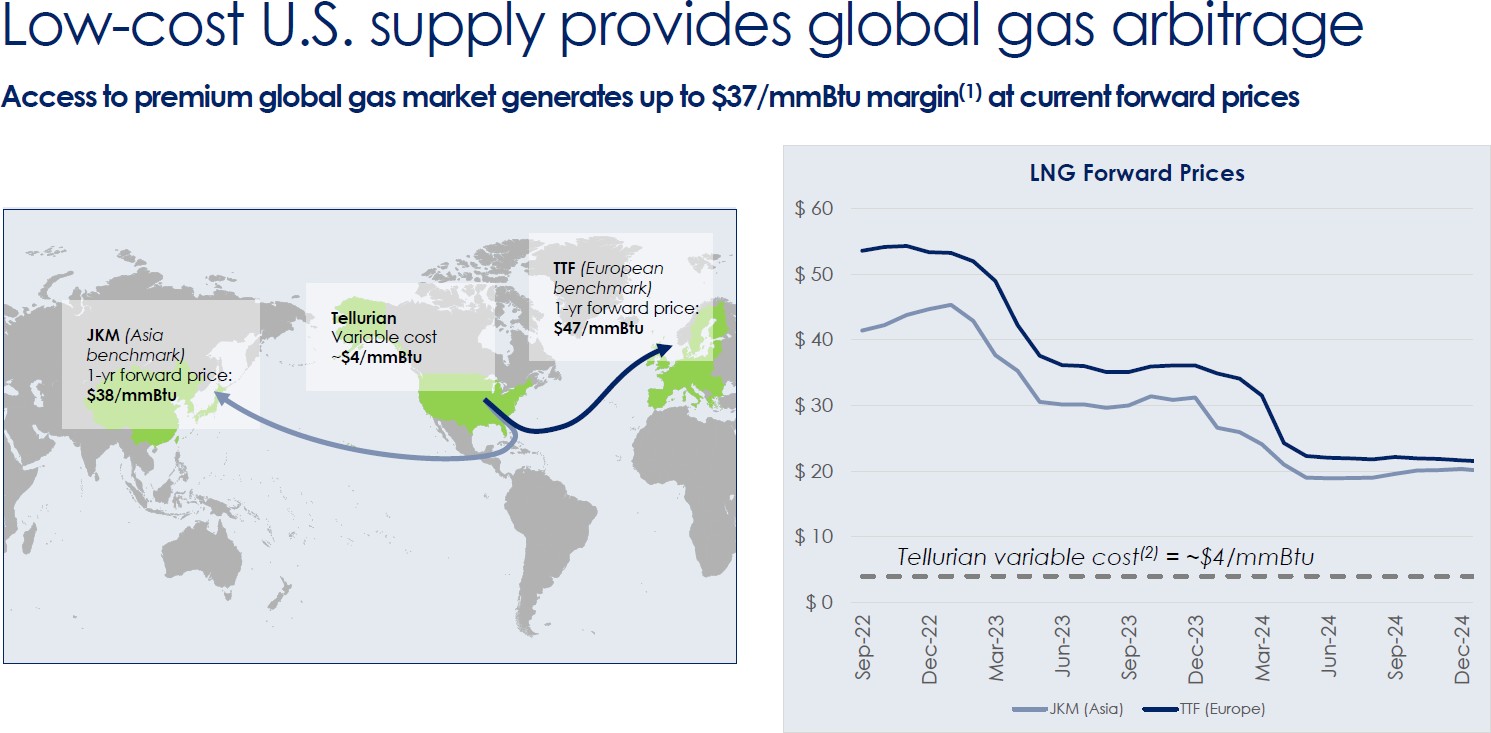

Due to Russia’s invasion of Ukraine and today’s energy crisis, which is especially severe in Europe, today’s $32.93/mmBTU Netback Margin (see chart below) is nearly four times the $8/mmBTU Tellurian has projected in the first chart which estimates $4 bn cashflow from Phase 1 and $11 bn cashflow from Phase 2. Tellurian’s funding prospects are aided in part by the Biden Administration’s commitment to deliver 50 BCF/yr to Europe by 2030 to replace Russian natural gas.

Source: Tellurian Investor Deck 8.2022

Because Tellurian’s Driftwood LNG is a high risk and high return project and due to recent years’ energy market volatility, TELL stock has been quite volatile. Charif Souki puts his money where his mouth is. He personally experienced margin calls in the 2020 COVID-19 market crash. Tellurian’s management owns 20% of Tellurian’s stock, so shareholders’ interests are aligned with management.

Source: Yahoo Finance

The Natural Gas and LNG Market:

The world has embraced climate change and UN Sustainable Development Goals and has sought to transition from fossil fuels to renewables like wind and solar. Unfortunately, this strategy and these goals have not been deployed uniformly and with limited success. In fact, before the February 24th Russian invasion of Ukraine, Europe was already engulfed in an energy crisis. Consequently, last year, Europe changed policy and proposed both LNG and nuclear as “transition fuels” to provide the needed energy for basic utilities at a reasonable price while the transition plays out over the decades ahead.

The energy crisis is global and not just European. Europe and North America enjoy high standards of living, but much of the rest of the world needs more energy for their economies to grow and converge toward our standards of living. 3.5 billion people globally do not enjoy continuous electricity. With UN Sustainability Goal #1 to end poverty and #2 to end hunger, there will be huge demands for energy in the future and natural gas looks to be the most compelling energy source during the energy transition of the coming decades. Doomberg a Substack periodical provides a funny balanced overview on the history on natural gas, LNG and reasons for its bright prospects.

The illustration below shows how cheap US natural gas can provide the world with needed energy while emits half the carbon emissions of coal and oil. The diagram on the right shows how the forward contracts point to lower future LNG prices that are comfortably higher than our first illustration that showed a $8/mmBTU margin generating $4 bn in cash flow per year.

Source: Tellurian Investor Deck 8.2022

Radical Decarbonization with Fossil Fuel Natural Gas:

Another powerful case for secular natural gas growth is made by the largest natural gas producer in the US, EQT Corporation. EQT argues compellingly that if we simply replace all the international coal production with natural gas, we could hit the decarbonization goals well ahead of 2050! Much of the global carbon emissions come from China and India which burn massive amounts of coal. If all international coal production was replaced with LNG, the world would hit our climate goals faster and without the devastating energy cost inflation plaguing the world.

The chart below details the LNG international coal replacement strategy advocated by EQT and others. This underscores the importance of LNG to the energy transition and the size of the addressable market.

Source: EQT Corporation Investor Deck

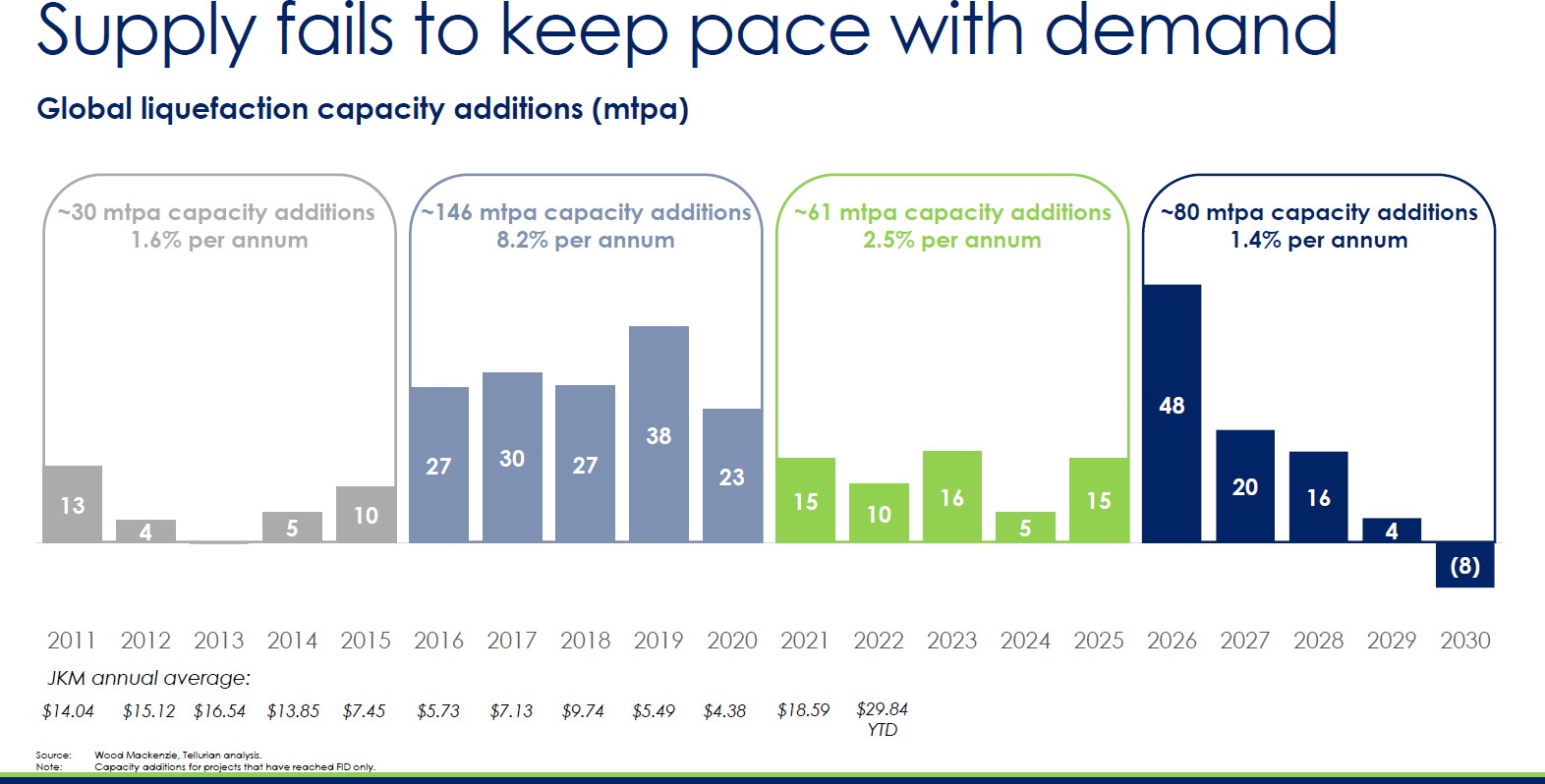

Currently the global liquefaction capacity growth projections suggest the market is early in its growth cycle. Further, the chart below shows that projected LNG production capacity is insufficient to meet future needs. The lack of new LNG projects suggests that future prices are not at risk of over-capacity.

Source: Tellurian Investor Deck 8.2022

Valuation and Souki History:

Tellurian Inc’s market cap is $2.34 billion, today, and share price $4.13. As of 6/30/2022, Tellurian’s common equity was $653 million and cash $823 million, so little of Driftwood LNG’s value is being attributed to Tellurian’s market capitalization.

When looking at Cheniere’s (LNG) long term stock chart, we observe that the Cheniere’s shares experienced their most rapid growth during the finance and construction periods. For example,

Cheniere’s first project was a gasification facility when the company was importing LNG and gasifying it. During that period, 2003-2005, Cheniere’s stock appreciated at 421% CAGR. Secondly during 2011-2014, Cheniere’s stock appreciated at 126.5% CAGR when Cheniere was building its first liquefaction facility and the company restructured to become a LNG producer and LNG exporter.

Consequently, we believe this financing period for Tellurian investors is as critical as was the case with Cheniere when it went through its financing and construction periods in 2003-2005 and 2011-2014. As the prospects for financing become a reality and the company becomes fully financed, Tellurian shares we believe could appreciate at similar abnormally high rates, if the company is successful.

The chart below of Cheniere Energy, Inc. (LNG) highlight the periods of unusual appreciation.

Source: IGA Yahoo.Finance.com

Charif Souki and Tellurian Inc. have seen wild swings. When Cheniere built its first facility, the plant was a degasification plant based upon high domestic US natural gas prices and low international gas prices. In the early 2000s, as fracking became widespread, the discovery of abundant associated natural gas in US shales changed the business proposition for Cheniere. This game-changing US natural gas discovery quickly reversed the economic proposition for importing LNG. From January 2008 to November 2009, Cheniere’s shares (LNG) plunged from $32.07/share to $1.78/share – a 94.5% decline in under two years.

Souki then restructured and redesigned Cheniere to convert low-cost US natural gas into LNG. This was a great challenge because while Cheniere was initially successful, Souki had to persuade his investors to reinvest in the massive new liquefaction facility. Souki succeeded with this monumental challenge.

Cheniere’s stock took off again rising to $83.59/share, from a low of $1.87 in 2009, before Charif Souki left the board in December 2015 due to a board fight with renowned shareholder activist Carl Icahn.

Financing Model Change:

Tellurian changed its financing model this year from “FID” Final Investment Decision to rolling funding. This financing strategy change frustrated shareholders and emboldened shorts. In late 2021, Souki had announced that Tellurian would announce their banking group by year end. The company has said that the financing would be 1/3 equity and 2/3 debt. Consequently, the announcement of a bank financing syndicate representing $8 bn in bank debt or placement capacity was viewed as a real positive step that did not occur. This may not have happened due to the company not acquiring enough Haynesville natural gas to secure that financing commitment. Early in 2022 Souki had projected that Tellurian would achieve FID in the first half of the year. With FID the financing is done and the Driftwood project is significantly derisked is simply a construction project. Many thought that getting FID would move TELL stock to the double digit price range and then the stock would commence a steady upward march, much like Cheniere’s stock did with its second financing run.

The other element was their equity finance side. Many thought that Tellurian’s only equity source was selling common stock. This simply was not true. That equity can come in a few different forms, whether it is upstream assets/cash flow, infrastructure investment (like the original Blackstone/Sabine Pass deal), a strategic investor (LNG offtaker or domestic E&P), or TELL stock (which is least favored and most dilutive.) These transactions can be complex. They can be done at the Driftwood level or at the Tellurian Inc. level. Consider Blackstone’s convertible deal with Cheniere in 2012: Cheniere Agrees to Sell $2B of Equity for Sabine Pass Liquefaction Project – Blackstone

Souki is a former investment banker and the management owns 20% of Tellurian stock, so we expect that Souki will look to use every viable option to pursue the least dilutive opportunity to raise capital. Consequently, using their own cash flow from upstream operations and or finding a strategic investor- customer would be the preferred route to financing, even if it takes longer and to the chagrin of retail investors.

On February 24th, the world changed with Russia’s invasion of Ukraine. Within a week of the Russian

invasion of Ukraine, Germany’s Chancellor Olaf Shulz reversed the country’s green policy, ordering the construction of LNG import facilities, terminating Nord Stream 2 pipeline with Russia, and sending weapons to Ukraine. Now Europe will need to replace 20 Bcf/d of Russian gas, the equivalent of c. 35% of the world’s LNG market. This led to a sharp spike in LNG prices and Tellurian’s stock in the six weeks following the invasion.

It seemed that Germany would quickly buy Driftwood’s offtake, but they did not. It appeared that Germany also sought to structure a deal with the Qatari’s but that also did not transpire. It seems that Europe’s plans to convert to hydrogen made some of these deals challenging. Asia does not seem so inflexible and that may be why we see the JKM marker used for cash flow illustrations even though the European TTF price is higher.

With the strengthening of the economy financing costs rose. With this year’s stunning energy crisis, opportunities for strategic investors grew following the Russian invasion of Ukraine. Domestic strategic investors also emerged as more compelling funding sources. Souki, in his informative two minute YouTube videos on the Tellurian website, explained on May 17th that several natural gas producers had expressed interest in gaining access to the international markets through LNG. https://youtu.be/wWGC6AV3pq4

Several public natural gas companies reported their interest in taking an equity role in LNG. Possible equity investors include: EQT Corporation (EQT), Chesapeake Energy Corporation (CHK), Comstock Resources Inc. (CRK), Devon Energy Corporation (DVN), Antero Midstream (AM) and Southwestern Energy Company (SWN). Souki said that the Cheniere Sabine Pass facility was first funded with the equity and then the banks followed.

We now believe that EQT Corporation the country’s largest natural gas producer would be a logical strategic investor in Driftwood. Furthermore, EQT just renewed a $2.5 bn five year line of credit and with the signing of the Inflation Reduction Act, the Mountain Valley Pipeline should make connecting the Utica and Marcellus shales in the North East with Driftwood more viable.

Additionally, Southwestern Energy Company (SWN), the largest Haynesville natural gas producer said in their conference call “We are evaluating on a risk adjusted basis, potential opportunities to benefit from global pricing by leveraging our approximate reliable long-term supply capability to help enable liquefaction projects to achieve FID”, Bill Way, CEO (SWN).

The New Milestone FNTP versus FID

One of the stories that the shorts were touting was that the SPA contracts of Vitol and Shell would expire on July 31, 2022, if a Full Notice To Proceed “FNTP” was not agreed to by Bechtel for Driftwood. (See page 21 under condition precedent.) That threat came and went. Amendments to the SPAs were announced and neither Vitol nor Shell cancelled thier SPAs. (See page 22.) Vitol and Shell own the LNG transport ships and charge a fee for their service, unless the project looked unlikely to succeed, why would they cancel these agreements if LNG is in great demand?

What became clear is that FNTP is more meaningful than the FID, in that if Bechtel commits to building the facility, then the prospect the facility being build is assured and the final elements of the financing are of secondary concern to Bechtel. Though FNTP financing required by Bechtel has not been made public, but it is less than the full FID of $12.8 bn.

If Tellurian raises $3.2 billion from strategics EQT and SWN with each contributing $1.6 billion each, then with TELL’s own $1 billion ($800 million cash and 200 million in cash flow), then the $4.2 billion in equity would be covered. Then Tellurian might raise $3-4 billion in debt through its bank syndicate. Souki had disclosed that they had signed over 50 NDAs signed with potential funders. Then Tellurian might have

$7.2-8.2 billion which might be enough for Bechtel’s FNTP milestone. But under NDA, Tellurian might be able to disclose funding sources like the EXIM bank which could provide guarantees for another $5 billion in debt or other financing options which would satisfy Bechtel.

Consequently, we believe that FNTP is the key milestone for Tellurian to derisk its stock and upon FNTP a share price close to $10/share or near analysts’ price targets for FID would be reasonable. With a higher stock price and a lower risk profile, with or without EXIM bank, Tellurian could achieve its FID as late as 2023, but shareholders will be rewarded for their patience as the deal would have been structured in the least dilutive way.

Recent News Supports Tellurian’s FNTP Pathway:

On August 3rd, Tellurian reported a 47% sequential increase in natural gas production. On June 1, 2022, Tellurian signed a $500mm convertible bond deal. In addition on July 13, 2022, Tellurian entered into an agreement to acquire additional Haynesville Shale land and production from Ensight strengthening its ability to self-fund.

On July 13, 2022 Souki made a thoughtful critique of the pay for service or toll road model versus Tellurian’s integrated model pointing out that Cheniere had to ask for an emissions waiver and the Freeport explosion show that there is little room for error in the traditional fee for service model Tellurian is seeking displace. https://youtu.be/HRztpzmzrJs

The fact Icahn Enterprise Partners, LP (IEP) recently sold Cheniere stock back to Cheniere is quite interesting, especially when Icahn stepped into Cheniere stock just as its development plans were materializing.

Tellurian is employing state of the art Zero Emissions technology and working with Bechtel, the EPC Cheniere used. We believe that many of the finance relationships that Souki forged while at Cheniere gives him a deep bench of funding prospects with whom Souki has credibility. We also like Tellurian’s institutional shareholders, some of who we consider among the smartest on Wall Street: Blackrock Inc., Paulson & Company, Inc., Shaw, D.E. & Co. Inc., and Citadel Advisors, LLC. Tellurian appears to be in good position to secure funding for FNTP and become a powerful growth story like Cheniere and an energy transition star.