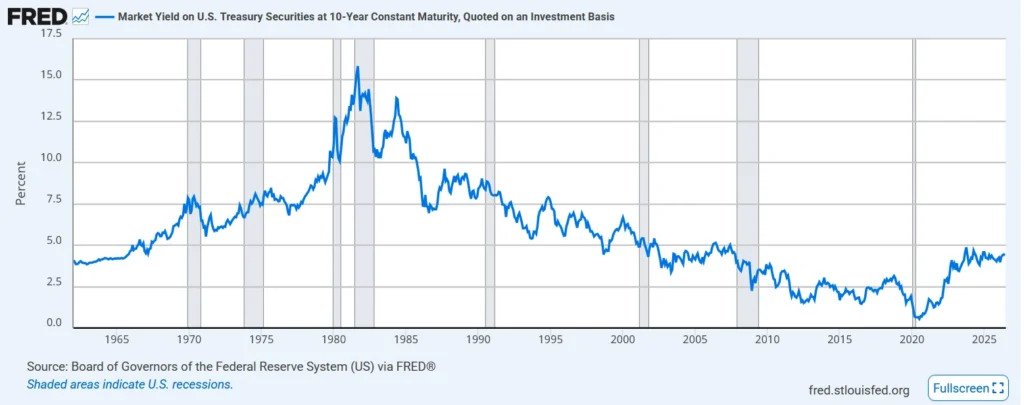

The great rotation theme we have referenced in recent years is based on changing fundamental factors like interest rates, inflation, geopolitical changes and historic analogues. We are moving from a unipolar world to a multipolar world where US military dominance is increasingly being challenged by China and others, and this is leading to slower growth and higher inflation than what we have been experiencing since the 1970s. Additionally, the secular decline in interest rates, which began in September 1981 when 10-year US Treasury yields peaked at 15.84% and bottomed in July 2020 at 0.55%, early in the COVID-19 collapse, has reversed, as shown in the chart below. These themes are detailed in a recent YouTube video with investment gurus Felix Zulauf and Jeffrey Gundlach.

We believe that inflationary and deflationary cycles — in combination with changing fundamental factors — provide powerful historic analogues to guide investment strategy today. The chart below of the S&P 500/PPI ratio suggests that we are now entering an inflationary cycle where commodities should outperform the S&P index for a decade long period. One of the clearest beneficiaries of this commodity cycle is gold and gold mining stocks due to a global financial system re-ordering due to excessive leverage and profligate government spending.

In the inflationary commodity cycle chart below, commodity cycles typically span 10 to 20 years and gold, energy, commodities, emerging markets outperform the S&P 500 and the dollar declines. In the 1970s and the 2000-2009 period, gold rallied about 10x and energy significantly outperformed as well. Due to the weakness of the dollar, which typically occurs during these cycles, investments in international and select emerging markets are excellent alternatives to large capitalization indexes like the NASDAQ 100 and the S&P 500 which now appear extended and overvalued.

Since 2019, Income Growth Advisors, LLC has been increasingly active in the gold and gold mining space. We now believe that gold is in a secular bull market fueled by global currency debasement and central bank fragility. Gold has recently experienced a 45% retracement of its gain over its March 2024 breakout move over $2075/ ounce.

The chart below of the VanEck Gold Miners ETF (GDX) peaked on March 2, 2026 at $117.18/share, at the start of the Iran conflict, and has retraced 54.33% of its rise over its August 2020 breakout above $43.23/share. Given the significant operating leverage that gold miners possess, if gold is bottoming or reversing its Iran War pullback, gold mining stocks are a compelling investment because they are fundamentally cheap with significant upside in these early years of a commodity super cycle. The GDX trades at a 14.7 TTM PE ratio with a 0.7% dividend.

With the Iran conflict deescalating and oil prices pulling back with the reopening of the Strait of Hormuz, we see Fed policy at peak hawkishness now with the arrival of its new chairman Kevin Warsh.

Druckenmiller Calls Gold Turning Point:

Stanley Druckenmiller is one of the greats, a former Soros protégé and sophisticated macro global strategist. Druckenmiller has recently posted several YouTube videos arguing that this selloff in gold is a normal reaction to a geopolitical event where energy is at risk. His historic analogue review YouTube cites how gold it the first asset sold by big institutional money, like foreign central banks, and these pullbacks provide insight into market behavior separate and distinct from fundamental and technical analysis that we incorporate in our thinking. These five global macro analogues are:

- 1973 when OPEC spiked oil 4x and the Yom Kippur war commenced;

- 1979 when the Iranian Revolution commenced and oil doubled;

- 1991 when Iraq invaded Kuwait;

- 2001 when the US was attacked on 9/11/2011 and gold rose from $290/oz. to $1826/oz. in August 2011 a 527% rise;

- and 2022 when Russia invaded Ukraine and gold rose 164%.

In each analogue, the first trade was to sell gold and buy US Treasuries for income and security. The buying of US Treasuries strengthens the dollar which makes gold less attractive for foreign holders and this prompts those foreign holders to sell more gold. After a few months, the dollar peaks, gold stops declining and central banks, who have been sellers of gold, reverse their selling and start buying gold again. Since 2022, central banks have been accumulating gold at record rates up until the attack on Iran. Now the foreign central banks who have been selling gold could soon flip become gold buyers again.

Below is a chart of the VanEck Junior Gold Miners ETF (GDXJ) which also is an equity proxy for gold with significant operating leverage. The (GDXJ) peaked on March 2, 2026 at $157.9/share, at the start of the Iran conflict, and has retraced 56.9% of its rise over its July 28, 2025 breakout above $66.23/share. Given the significant operating leverage that junior gold miners possess, junior gold mining stocks are particularly compelling investments in these early years of a commodity super cycle. The GDXJ trades at a 13.9 TTM PE ratio with a 2.24% dividend.

To get diversified exposure to the gold sector, we like owning GDX and GDXJ and would buy those VanEck ETFs today. However, we see enormous upside in two microcap stocks:

Blue Lagoon Resources, Inc. is poised for a valuation re-rating due to its achieving commercial production on May 19th with 100 tons per day of ore production, its steady growing production prospects, and its 57.5% share price decline since its January high. Having attended Blue Lagoon’s mine opening ceremony in British Columbia in July 2025, we have developed a deep understanding of gold mining and Blue Lagoon’s operations and progress. As a new cash-flow generating debt-free high grade gold mining company, we see deep value that the market has yet to appreciate because its mining success has not yet flowed through into reported earnings. This gap between knowing what the company is worth, through thorough research, before those financials are reported, is the essence of successful research-based investing. Our research suggests that the company is generating about $2 million in cash flow per month (an annualized $24 million rate) and should grow to $3 million in cash flow per month (an annualized $36 million rate) for a company with a $71.14 million market capitalization.

Gold mining market capitalization to cash flow multiples are 7 times, per seeking alpha database. This implies that Blue Lagoon could trade to a market capitalization of $168 million based on 100 tons of ore mined per day and $252 million based on 150 tons produced per day expected in coming months. Assuming 150 million shares outstanding, BLAGF shares should trade to $1.12/share and to $1.68/share. This seems like an achievable range this year if we get a turn upward in the price of gold that we anticipate.

Furthermore, BLAGF hopes to commence drilling in September. Drilling is the part of a miner’s lifecycle (aka Lassonde Curve) when the greatest upside appreciation occurs. Blue Lagoon should commence infill and exploration drilling in September. Based on $200/oz. for gold in the ground, if Blue Lagoon is able to prove out its estimated one million ounces of gold around the Boulder Vein within the next year, $200 million in resource value could be added to Blue Lagoon’s balance sheet. In addition to that anticipated one million ounces of Boulder Vein gold, 15 new undrilled veins are located nearby, and Blue Lagoon’s unexplored 18-kilometer strike offers enormous upside that is not reflected in the company’s current valuation. This 18-kilometer strike was specifically mentioned by a major gold mining company which met with Blue Lagoon at the Beaver Creek Precious Metals Mining Summit last September. Michael White, President and CEO of IBK Capital in Toronto Canada, said that I might be right and the shares could rally to $1.5 on mining operations, but “a few good drill holes” could lead to BLAGF shares shooting to $3 to $4/share based on drilling results. From $0.47/share, we remain quite sanguine on Blue Lagoon shares.

Nicola Mining Inc. (NICM) in Merrit, British Columbia is a miller or ore processor that takes Blue Lagoon’s ore production, processes it and sells that residual concentrate to Ocean Partners. Nicola Mining has partial ownership of three mines: New Craigmont Copper Project, Treasure Mountain Silver Project, and Dominion Creek Gold Project. CEO Peter Espig is a former Goldman Sachs investment banker who I met last July at the Blue Lagoon Mine Opening Ceremony. As a miller, NICM, is less susceptible to the boom busts operating profiles that miners can experience, but as a shareholder in Blue Lagoon and processor with other mining project prospects, NICM is an attractive investment that is more diversified than Blue Lagoon.

In a phone interview with Espig last week, Nicola looks to enjoy a healthy ramp in earnings as it has prepaid nearly $10 million in expenses, which, as operations engage, mean the company will enjoy margins that should be $10 million higher than production estimates would otherwise suggest. More importantly, its Dominion Creek Gold project looks to be a solid revenue generator for Nicola in 2026.

Furthermore, Nicola’s Treasure Mountain Silver Project has 450,000 ounces of silver it expects to mine over the next four years, and given that the company believes its mining expenses will be paid by the lead and zinc produced by the mine, silver revenues could soar if silver gets to $100/ounce or multiples of that if some bullish silver projects materialize.

Nicola Mining has a $107 million market cap, has 210 million shares, is not profitable and was recently listed on the NASDAQ. Below is a chart of Nicola Mining traded on the NASDAQ since April.

Conclusion:

We believe that we are headed into an inflationary cycle where commodities should outperform the S&P 500 meaningfully as they did during the 1970s and the 2001-2009 inflationary cycles.

While the crowd is clamoring over SpaceX and AI hyperbole, we believe that the pullback that gold has experienced this year is a rare opportunity to buy premium assets following a 45% decline for gold and 55% decline for gold miners from their breakout levels. If our thesis plays out, gold should bottom here based on the historic analogues and equities should underperform if not struggle in the years ahead especially in comparison to gold or gold mining stocks.

For cautious diversified exposure we like GDX and GDXJ, but for investors looking for material upside, we see Blue Lagoon (BLAGF) as exceptionally cheap with massive resource potential and Nicola Mining (NICM) secondarily.