When markets feel euphoric and US equity valuations are near record highs, reducing equity exposure is prudent. Allocating to high growth gold mining stocks seems timely as we reallocate toward inflationary cycle beneficiaries like commodities, gold, silver, energy, value, small capitalization stocks, emerging and foreign markets.

Today’s market extremes are highlighted by the chart below from Andrew Sarna’s, Off the Charts.Substack.com newsletter. The chart captures the risks of today’s AI euphoria, SpaceX excitement, and record stock prices. A five standard deviation move is a one in 3.5 million event and reminds sober investors of the wisdom of the selling high and buying low investment strategy. Veteran investors like Income Growth Advisors, LLC, understand the benefits of a contrary investment strategy and recommend trimming parabolic, AI, and technology stocks, as well as selling large cap indices like the S&P 500 and NASDAQ 100. We believe that the wildly anticipated IPOs of SpaceX, Anthropic, and Open AI may mark a speculative peak for this market cycle, and we advocate diversifying into value investments and away from today’s most popular investments.

The one in 3.5 million odds of the momentum versus minimum volatility index ratio charted below by Alpine Macro suggests taking defensive steps.

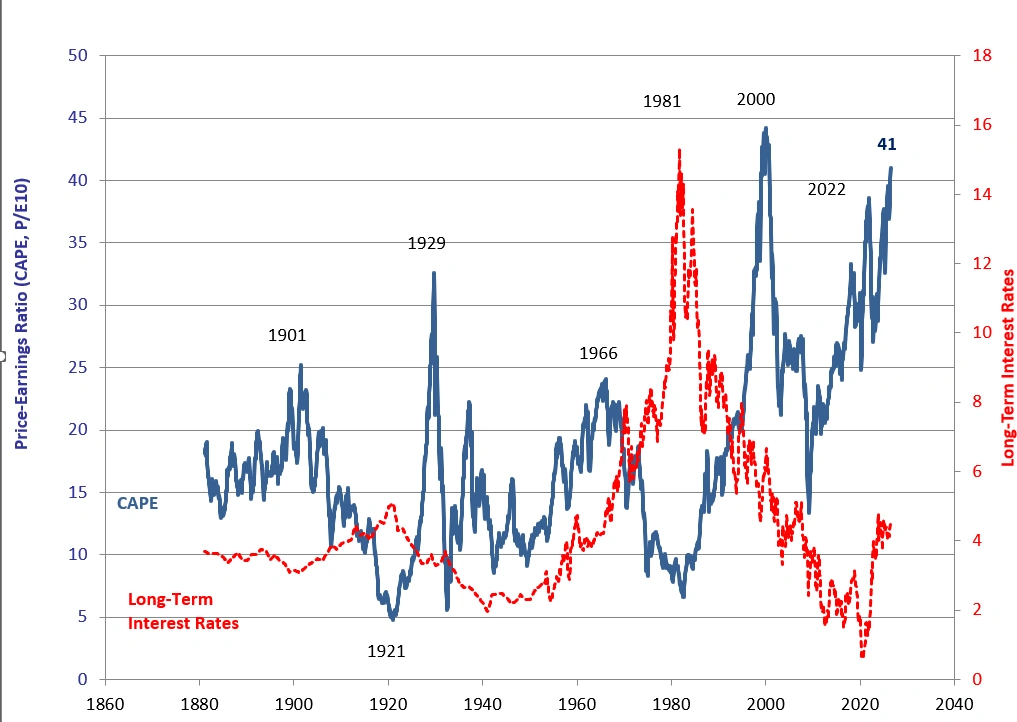

Similarly, today’s Cyclically Adjusted PE (CAPE) ratio developed by Nobel Laureate Robert Shiller is at 41.02. Today’s CAPE is the highest level since 2000, during the Tech Bubble, which stands among the three peak high valuation levels in 1929, 1966, and 2000, which have preceded three of the worst market declines in history.

We believe historic market cycles and analogues are valuable guides to investing. The history of inflationary and deflationary cycles since 1885 provide thoughtful economic and market analogues sensitive to inflationary trends.

We believe we are entering an inflationary cycle, and we should expect the S&P 500 and bonds to underperform over the next decade, as an inflationary cycle unfolds, and outperformance will likely to be in small capitalization and value stocks, emerging market and foreign geographies, cash, and commodities in energy and precious metals, in particular. The next decade will likely resemble the 1970s, the 1999 to 2009 period, and the Great Depression.

Gold Is The New Top Global Reserve Asset!

The ECB recently reported that gold has replaced US Treasuries as the world’s leading reserve asset. Reserve assets are liquid assets managed by a country’s central bank. The fact that gold is now the largest reserve asset in the world shows that not only are finances of the United States in a precarious state, but so are the finances of Japan, Italy, France, Germany….

The importance of this milestone is that the world’s most sophisticated investors are more confident today in gold than in US Treasuries. This fact strengthens our belief that gold could be in a secular bull market or super-cycle where gold prices could rise as high as Pierre Lassonde’s $17,250 target in 2032. While recency bias will keep most investors trapped in a 60-40 portfolio allocation, allocating to gold, silver, precious metals and their miners could be a shrew way to reallocate into good investments which could provide significant return prospects if our gold and commodity thesis play out over the years ahead. I used to be skeptical of Princeton Economics Professor, Jeremy Siegel, when he first started publishing his stock market predictions, but now feel that Pierre Lassonde deserves the same respect that Professor Siegel does.

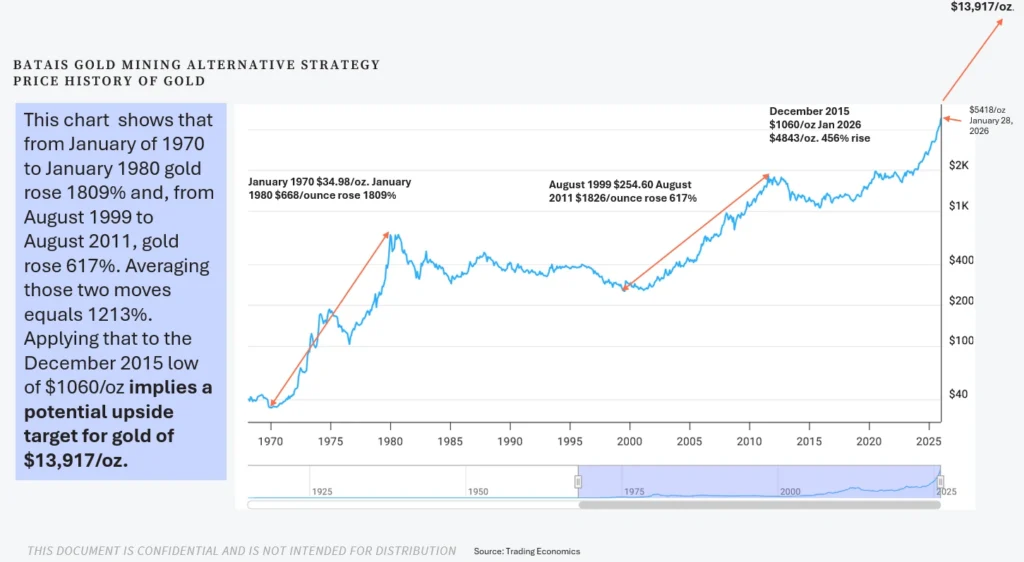

Based on past gold cycles we believe that gold could potentially move substantially higher based on the 1970s move and the 1999-2011 move and could reach $13,917/ounce based on the last two cycle moves. We believe we are currently in a mid-cycle consolidation like 1974-1976, and gold is consolidating its $2000/ounce to $5400/ounce move.

“Furthermore, following Russia’s invasion of Ukraine and US seizures of Russian assets, countries adversarial to the US, like Russia, China, North Korea and Iran, find it compelling to buy gold versus US Treasuries to retain political and financial independence from the US. Until imperialistic behavior by Russia, Iran, and China cease, gold should have a consistent bid. Furthermore, de-dollarization is a growing trend where BRICS (Brazil, Russia, India, China, and South Africa) are seeking dollar independence in their international trade activities and increasing demand for gold at the expense of US dollar and US Treasury dominance.

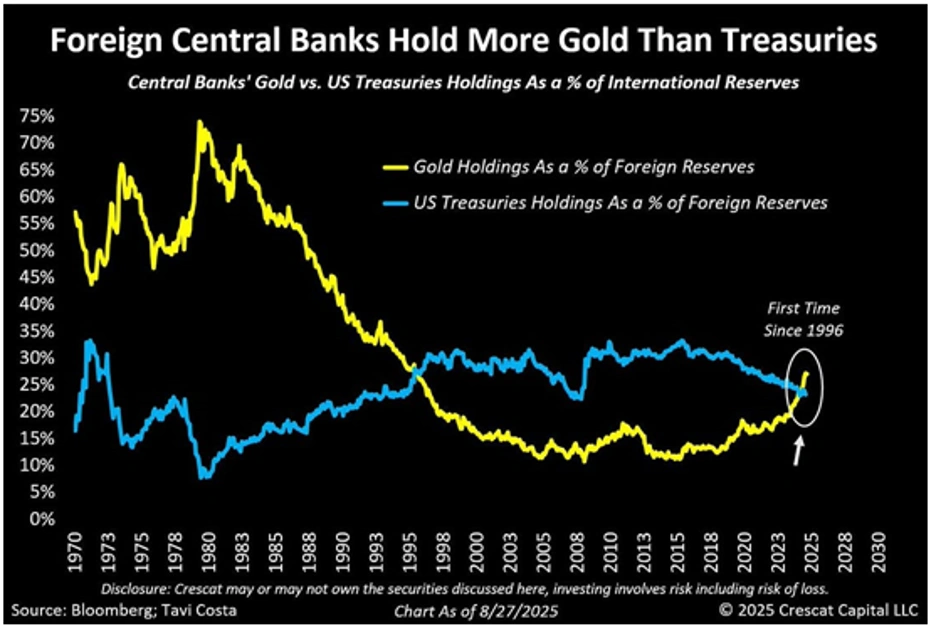

The chart below shows the percentage of foreign central bank ownership of US Treasuries versus gold. This chart shows gold holdings, as a percentage of International Reserves surpassing US Treasuries for the first time since 1996. We foresee this trend persisting which will be supportive of gold.

Monetarily, gold is increasingly being seen as the predictable international currency in a period where fiat currency risks are rising. We see gold being viewed as a steady predictable currency when confidence in crypto and traditional currencies are losing popularity.

Another driver of demand for gold is the increased percentages of gold in asset allocation models recommended by top investment strategists like DoubleLine, CEO Jeffrey Gundlach and Bridgewater Associates, Founder, Ray Dalio, who are now making the case for a 20-25% allocation after years of low single digit allocations. A similar systemic reallocation could lead to a four-fold increase in gold and gold miner ETFs over the years ahead.

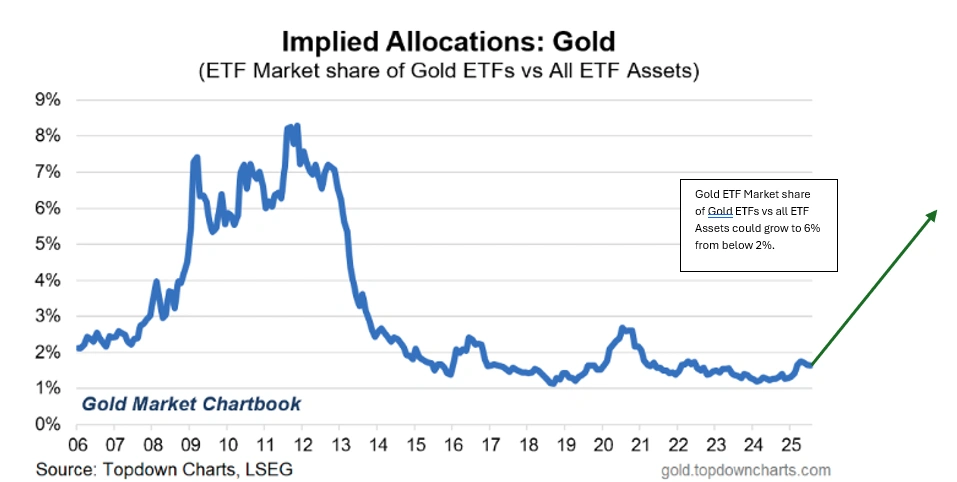

The chart below of the percentage of Gold ETFs versus All ETFs, shows an approximate 75% decline in weightings from 8% to 2% since gold’s peak in 2011. Since we believe that we are in a secular gold and commodity cycle, we anticipate a decade of upside for gold and gold mining stocks with many folds of potential upside.

Another driver of gold and gold miners is quantitative momentum, which dominates nearly 80% of exchange volumes today. Combined with gold’s low and occasional inverse correlation to equities, gold should experience persistent demand in portfolios and asset allocation models the years ahead.” Tyson Halsey, CFA Seeking Alpha

The Case for High Growth Gold Mining Stocks:

Historically, investment giants Warren Buffett and John Bogle have argued that gold is a non-productive asset. While gold historically is valued for jewelry, currency, and a store of wealth, gold mining stocks generate revenues, cash flow, and earnings, unlike the yellow metal. As such, we believe that gold mining stocks should outperform gold in the years ahead.

Below are three growth gold mining investments we recommend with increasing levels of risk:

“VanEck Junior Gold Miners ETF (GDXJ), is an ETF investing in growth gold miners. The diversified structure reduces single stock risk and offers the benefits of owning growing gold miners during a gold bull market. With a modest dividend and 16.5 times trailing earnings, GDXJ is a lower risk way to play the high growth portion of the gold market.

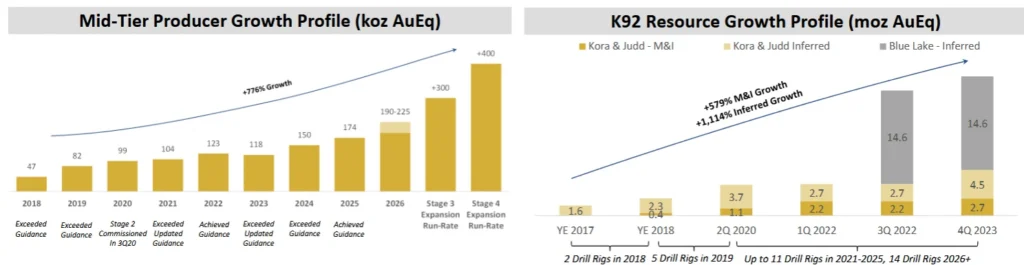

K92 Mining Inc. (KNTNF) is a $4.3 billion market capitalization gold miner in Kuala Lampur. Quinton Hennigh, PhD., the geologist who led Crescat Capital to fund Blue Lagoon’s resource development, believes K92 Mining Inc. is the best example of Blue Lagoon’s potential growth in the future. KNTNF has a massive carbonite type gold deposit associated with some of the largest resources in the world. KNTNF resides in Papua New Guinea near Australia and close to Porgera Gold Mine a top 10 producing gold mine globally. The diagrams below from it investor packet reflect its high growth track record.

Blue Lagoon Resources, Inc. (BLAGF), a newly restarted $90 mm market cap gold miner in British Columbia, Canada is our most speculative high growth gold mining investment idea. BLAGF recently announced having attained commercial production of 100 tons of ore per day. We view the purchase of CN$3 million in equity by Ocean Partners, its concentrate off taker, at CN$0.90/share (BLLG.CN) as confirmation of insightful professional investment at current market prices.” Tyson Halsey, CFA, Seeking Alpha.

We chose K92 Mining Inc. and Blue Lagoon Resources, Inc. because these companies own alkaline-associated gold resources which can be massive scale and high-grade resources and because Quinton Hennigh, PhD., who helped Crescat Capital fund Blue Lagoon 2022 resource development has spoken favorably about Blue Lagoon’s potential massive scale and that K92 is a good potential comparable for BLAGF.

The 7-year Chart below of Blue Lagoon shows its shares are trading at $0.56/share, well below its near IPO high of $1.45 in 2019. Inlight of the resource development which has occurred since 2019, its recently achieved commercial production status, and the resource value generation potential from Blue Lagoon’s cash flows, we would capitalize on recent price weakness to accumulate BLAGF shares.

The financial leverage of a growth gold miner is reflected below in our Blue Lagoon Resources summary:

BLAGF announced on it had achieved commercial mining status on May 19th, 2026. Commercial production marks the official operating status transition from a resource company to one which is steadily generating cash flows. Based on 100 tons per day, our rough estimate is that BLAGF should generate about $2 million in cash flow per month and, with 150 tons per day of production per day, should generate $3 million in cash flow per month. Assuming annualized cash flows $24 million to $36 million per year and a seven-times cash-flow-multiple, Blue Lagoon Resources should trade to a market capitalization of $168mm to $252mm, assuming BLAGF exits the year producing 200 tons per day. Given today’s 150,000,000 shares outstanding, BLAGF shares should trade between $1.12 – $1.68/share, before a premium starts to be factored in for resource value added from infill and exploratory drilling in September 2026.

Blue Lagoon’s mining cash flow generation should value the company near $1.40/share this fall, before the infill and exploration drilling resource value drivers begin being added to the mining-cash-flow multiple valuation. Specifically, as infill drilling begins to prove out, an estimated upwards of one million ounces of gold in the ground could be added by April 2027. The chart below shows and link detail the 15 veins that Noranda identified in the 1985-1993 period and spend $60 million on, illustrates how the Boulder vein infill drilling could yield one million ounces of gold in the Boulder Vein area by spring 2027. Assuming an “in-the-ground-valuation of $200/ounce”, $100 – $200 million in resource value could be added to the market capitalization. The 15 veins are not part of the projected one million ounces BLAGF hopes to certify over the next year.

The third value driver, also funded by mining cash flows, will be from the exploration of the Chance Structural Zone or the 18 kilometer strike. This 18 Kilometer strike (9:00 minutes) was highlighted by a major gold ming firm in Beaver Creek last September.

To grasp the upside as the Blue Lagoon gets into the exploration stage of resource development, we hosted Michael White, CEO and President, of IBK Capital in December 2025, on a zoom call. White states that, over the next few years, BLAGF could certify upwards of 5 million ounces and at $200/ounce, could have a market capitalization of $1 billion. Furthermore, if its share count expands to 175 million shares, BLAGF shares could rise to $5.50-$6.00/shares. We believe that if over the next year, if Blue Lagoon hits a few good drill holes it could jump to $3-/4/share in 2027.

Conclusion:

While Friday’s NASDAQ 4% decline, left gold and gold mining stocks under pressure, we believe we are in the early stage of a secular inflationary cycle where commodities and gold will increasingly replace bonds and stocks in asset allocations for the next decade. Based on JP Morgan, Jeffrey Gundlach, and Ray Dalio’s recent commentary, we see steady support for gold and gold miners in the years ahead. Furthermore, the eroding confidence of the finances of the United States, Japan, Italy, France and Germany, will lead to more central bank gold purchases to defend against debasing currencies globally. This central bank trend has grown so prevalent that gold is now the largest reserve currency in the world.

While gold, as a commodity, has little productive value, gold miners are cash flowing revenue producing enterprises and should enjoy considerable operating leverage as they will be able to explore, develop and mine in the years ahead. For newer productive gold miners, the potential for outsized gains should be seen in K92 Mining, Inc. and Blue Lagoon Resources, Inc., and the VanEck Junior Gold Mining ETF for more cautious investors. While we are keen on growth gold miners, these are not the only investments which should do well over the next decade. Small cap, value stocks, foreign and emerging markets should also provide value not readily available in the S&P 500 and NASDAQ 100. Our preference for Blue Lagoon comes as a result of our visit to Blue Lagoon’s Mine Opening Ceremony last July 7-10th which allowed us to meet Blue Lagoon’s investors, engineers, employees, and analysts, tour the Dome Mountain mine, and develop an in-depth understanding of gold mining valuation analysis and gold mining.

We believe today’s stock market exhibits the exuberance often seen during bubbles like 2000, 1966, and 1929, and macroeconomic challenges like those in the 1970s. Though we cannot specify when a market top will occur, we believe that transitioning into a 25% cash, 25% commodity, 25% bond and 25% stock asset allocation will provide a far more compelling risk reward profile, especially to retirement aged and retired investors, than can be generated from the popular 60-40 stock bond asset allocation model popularized in the 1970s and 1980s. We believe that a 60 S&P 500 and 40% 10-year US Treasury fund would be vulnerable to inflation, war, and recession, with higher risk and lower income than a 25% cash, 25% commodity, 25% bond, and 25% stock allocation for the next decade.