The current rise in NVIDIA Corporation (NVDA) shares, mega cap stocks, and capitalization weighted indices, has all the markings of a generational stock market peak like 1929, 1974, and 2000. Like past historic bubbles, the current market is manifesting a parabolic ascent, historically high valuations, and an “irrational exuberance” based this time on the extraordinary growth expectations for “AI” (artificial intelligence). The psychology of fear and greed are repeated throughout history. Academics have chronicled how the psychology of crowd behavior in boom and bust cycles throughout history remains constant regardless of the bubble asset, whether it is tulip bulbs, real estate, commodities, or equity markets.

Humans are herd animals. When the current extraordinary ascent reverses, crowd psychology, and market history lead us to believe a bust in the AI exuberance and a crash in mega cap stocks will ensue. We think a market decline on the order of 80%, 83% and 52% could ensue for NVDA, the NASDAQ, and the S&P 500 respectively once this market peaks, because those were the respective declines following the 2000 bubble experienced by CSCO, the NASDAQ, and the S&P 500.

Investing Through a Market Bubble:

This is a moment when all investors, especially those heavily invested in equities should consider reducing equity exposure to 25%, bond exposure to 25%, raising commodities to 25%, and keeping 25% in money markets and two-year Treasury notes. Reductions in market capitalization weighted indices, equity ETFs, and equity mutual funds, are especially important because these investment vehicles have grown to be overly popular and are beneficiaries of the boom in passive asset allocation in recent decades. Investors in the popular 60% equity 40% bond asset allocation model could experience a 30-50% loss in the coming months and years despite financial planners and asset allocators pointing to their attractive long term records. Unfortunately, over the last fifty years, asset allocation and investment management have evolved to overweight momentum investing and mega cap stocks despite numerous equity market indicators showing historic overvaluations.

These facts have created the risk of a generational market decline like 1929, 1974, and 2000 in the months and years to come. Older managers and students of market history will note that today many investment managers and investment company directors have not invested through a generational decline when conventional investment policies and strategies implode.

Three Historically Overvalued Equity Models:

Below are three quantitative measures which show near record historic equity market valuations. These are long term models which help to remove recency bias.

Robert Shiller’s Cyclically Adjusted Price to Earnings “CAPE” ratio quantifies extreme market valuations over the last 140 years, specifically, 1901, 1929, 1966, 2000 and today. The chart below shows the current CAPE reading of 35.5 exceeds the peaks of 1901, 1929, and 1966, periods that preceded protracted bear markets.

Warren Buffett’s so called “favorite indicator” compares the ratio of the Russell 5000 to the US GDP. The chart below shows the Buffett valuation indicator is currently 188%, a ratio that is two standard deviations above normal and comparable to the levels reached in the equity bubbles of the late 1960s and 2000.

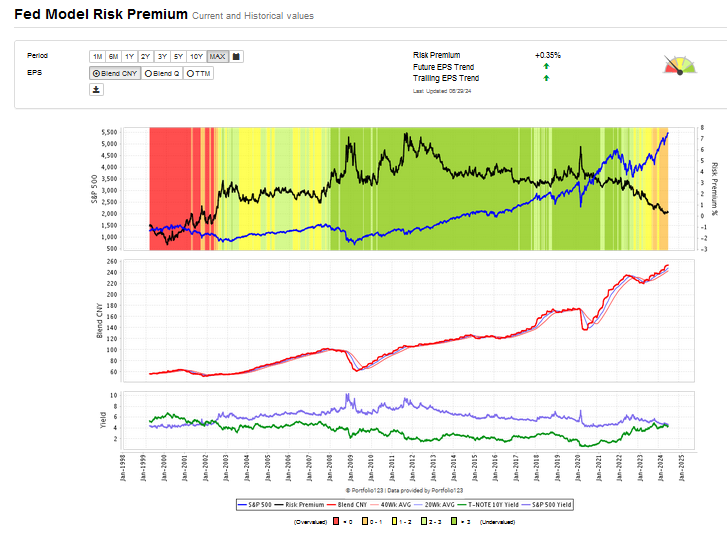

The Fed Model or Risk Premium model shown below compares the S&P 500’s earnings yield (currently 4.63%) to the 10-year US Treasury note’s yield (currently 4.43%) and shows a meager risk premium of only 0.35%, a level not seen since 2002.

What would really reduce the risk premium into a perilous risk range would be a further rise in interest rates (likely driven by inflation) or a decline in earnings from an economic slowdown.

A-Irrational Exuberance:

- NVDA’s $3.35 trillion market capitalization reached on June 18th has surpassed AAPL and MSFT.

- Nvidia’s market capitalization spike has helped lift the NASDAQ 100 and S&P 500 market capitalization weighted indexes to new highs as well.

- Parabolic moves generally don’t end well. Fear of missing out or “FOMO” creates panic buying and an unsustainable pace of price appreciation.

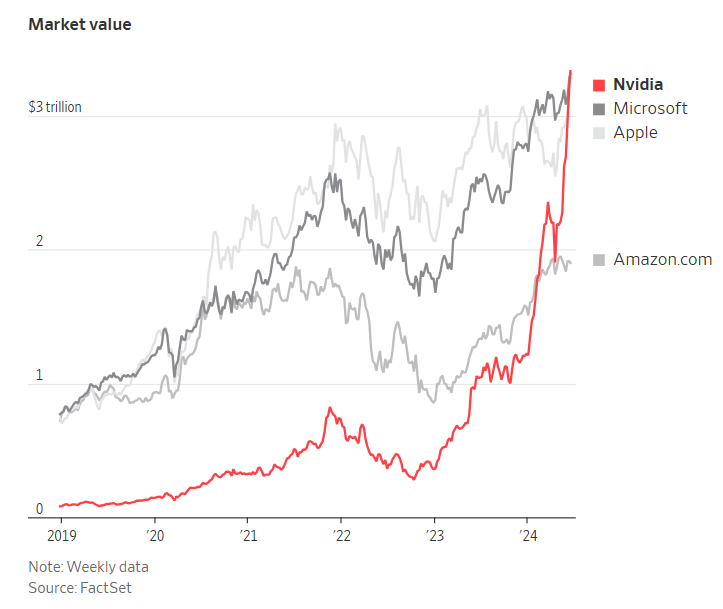

Below is a chart of the market capitalization of NVDA and how, since the launch of Chat GPT, its market capitalization has soared past the market caps of Microsoft, Apple, and Amazon. The rapidity of NVDA’s rise is unusual and now at a potential breaking point.

NVDA rose from $11.22/share on October 14, 2022 to $135.58/share on June 18, 2024, a rise of 1108% or (11x) in 20 months.

Chat GPT launched in November 2022 and inspired the public’s investment imagination that created this current euphoria and irrational exuberance in NVDA shares.

The NVDA Bubble:

Bubbles are most clear when they are shown over the long term and when compared to another economic metric. The chart comparison below of Cisco Systems, Inc. (CSCO)’s bubble in 2000 to the Nvidia Corporation (NVDA) bubble in 2024 juxtaposes the two parabolic market capitalization ascents of each company relative to the US GDP. Not only is NVDA’s ascent far more rapid, NVDA market capitalization peaked as a percentage of US GDP at 11.7%. This is far more extreme than CSCO’s market capitalization to US GDP of 5.5% in 2000. NVDA may prove an extraordinarily profitable short between now and year end.

While bulls say NVDA’s ascent is deserved because of its extraordinary earnings growth, we disagree. While Nvidia’s earnings per share quintupled its fiscal January 2023 and earnings per share estimates should double in the current fiscal 2025, a sharp earnings deceleration can prompt a pe multiple collapse. Stock guru O’Neil used sharp earnings deceleration as a sell signal.

The law of large numbers will prevent NVDA from continuing to grow at this extraordinary pace. Once NVDA’s earnings growth stops surprising to the upside and its earnings growth moderates, a rapid share price decline will ensue. In the next two quarters, we believe momentum traders and FOMO traders will start dumping their shares and then the positive feedback loop which drove NVDA’s miraculous rise will reverse and lead to a swift decline like CSCO’s shares experienced in late 2000.

The table below of Nvidia’s Revenues, EPS, and Net Income show a pronounced deceleration in earnings per share growth from 561% to 128% and net income from 581% to 113% from fiscal 2024 to fiscal 2025. O’Neil and other quantitative analysts know that a rapid deceleration in earning growth can lead to a multiple collapse and a share price decline that can be devastating.

For speculative investors, an investment in Graniteshares 2x Short NVDA Daily ETF (NVD) may be an attractive trading vehicle to capture the decline we foresee for NVDA later this year. If NVDA’s shares decline 50%, NVD is designed to double if NVDA’s shares decline 50%.

The Mega Capitalization Stock Bubble:

The bubble in mega cap stocks is brilliantly displayed in the chart below of the 10 largest market cap stocks in 2024 and juxtaposed to the 10 largest market cap stocks in 2000 on a 24 year phase shift. We believe a sharp decline in many of these large capitalization growth stocks is likely as we head into the yearend. A decline in Nvidia could hurt other expensive mega caps. If the selling of NVDA shares begets selling in other mega cap stocks, then the NASDAQ 100 could turn south and a negative feedback loop of index selling driving mega cap stock selling could creates more index selling prompting more mega cap selling…. A break in NVDA could easily trigger a feedback loop of selling and turn capitalization weighted indices into a bear market rout as equity market valuations are near historic highs.

The potential market rout we envision could easily be capitalized on via inverse ETFs on the NASDAQ QQQ like the ProShares UltraPro Short QQQ (SQQQ). But for an opportunity like this to prove highly profitable, earnings or revenue growth need to slow or turn negative in the months and years ahead.

The chart below of the 2000 and 2024 mega cap bubbles presented side by side shows the uncanny correlation of mega cap price behavior to other mega cap stocks. We remember the decline in the market from 2001 to 2003. It was sharp and persistent after years of positive upward momentum in large cap technology.

In the late 1990s, I had run Helsinki Advisors, LLC a top performing tech hedge fund and cut back sharply all my tech exposure at the market peak in late March 2000. Despite a timely exit, I was drawn back into the stock market. I was still a prisoner of recency bias. I kept looking back to old market leaders for success, and that strategy was a mistake. Once a bubble bursts, it takes years for the market to adjust. With the benefit of hindsight, I came to realize that by investing from 2000-2010 in unpopular markets, assets, and sectors like the emerging markets, energy, commodities, small cap stocks, and value stocks, I could find meaningful opportunities for high returns in new markets. For this reason, we suggest a 25% allocation to commodities which is a significant deviation from 60% equity 40% bond asset allocation popularized over the last 50 years.

The Nightmare Scenario:

To understand the vulnerability of a major market top and bear market we look to both historical analogues and fundamental factor vulnerabilities.

In the 1960s and 1970s, the Federal Reserve had to fight inflation due to excessive government spending, the Vietnam War, and the spike in oil prices due to the OPEC oil embargo. In the mid-1970s, the Federal Reserve claimed victory in fighting inflation and then, under Fed Chair Arthur F. Burns, began easing monetary policy. This premature easing, before inflation was soundly defeated, led to a spike in inflation and interest rates and a persistent bear market in stock prices. The equity bear market ended in the early 1980s after Paul Volcker raised Fed Fund rates to 20% and the inflationary spiral of the 1970s ended. The economic malaise of the late 1970s led to the considerable unpopularity of President Jimmy Carter. Paul Volcker successfully broke the back of inflation through restrictive Fed Policy, but the Fed’s failure to control inflation in the late 1970s left an indelible economic memory of stagflation where both high inflation and high unemployment created economic misery.

The chart below of the Fed Funds rate shows that in the late 1970s Fed Funds rates rose to stanch resurgent inflation. Many stock market commentators are forecasting a cut in Fed Fund rates later this year, but economic historians will point to the 1970s experience to assert the risk of prematurely easing interest rates without having sustainably reduced inflation to 2%.

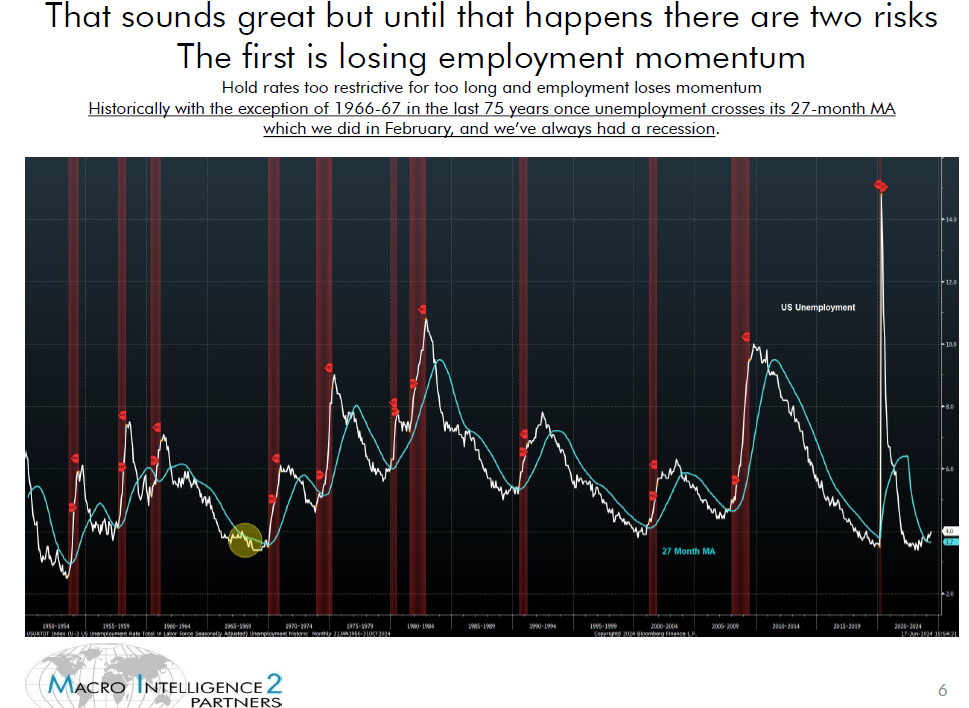

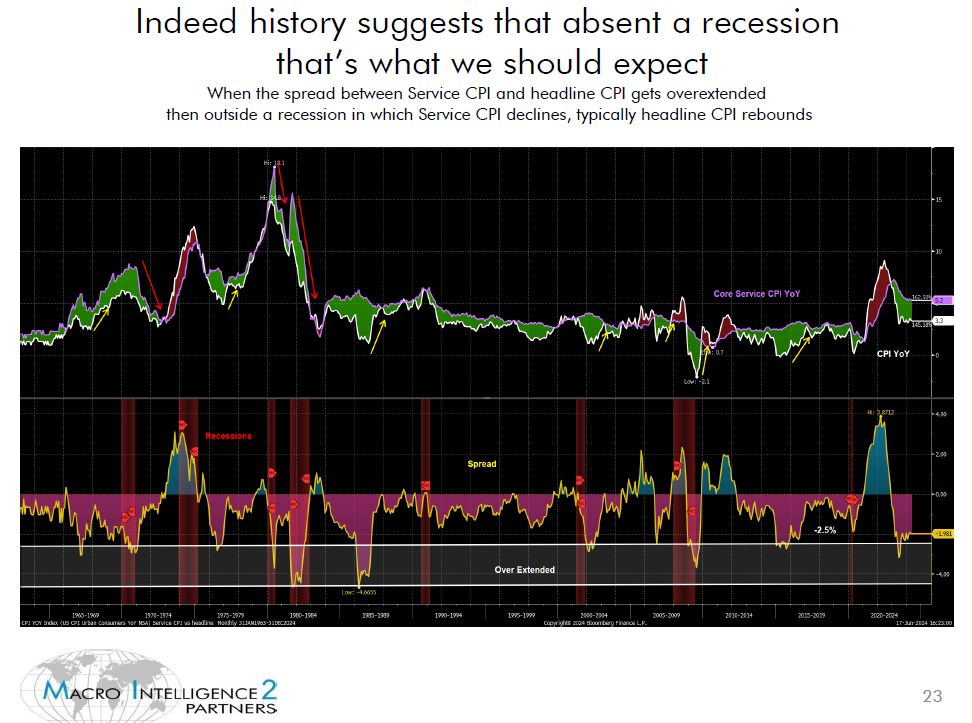

A recent presentation by Macro Intelligence 2 Partners caught our attention because they showed economic pathways to higher inflation or higher unemployment. Either higher inflation or an economic slowdown could turn the risk premium negative and signal perilous overvaluation like that in 2000. Below are three charts outlining possible economic risks which could lead to a generation market decline. The two risks markets want to avoid are inflation and recession.

The chart below of unemployment shows that we are on the precipice of a recession and that the unemployment rate is rising above its 27 week moving average, a signal highly correlated with the US entering into recession.

The risk of inflation is that while the CPI has declined, services inflation remains stubbornly high near 5% and this will likely lead to the CPI rising in the coming months. Higher inflation will lead to tougher monetary conditions and pressure the US equity markets.

The worst case scenario for the equity markets would be meaningfully higher interest rates. MI2’s demographic model below suggests that we are in a bond bear market and that even in a recession, long term treasury yields will only drop to 3%.

With US Treasury debt exceeding the US GDP and interest coverage expense of our debt now exceeding US military outlays, the government bond market is in bad shape and recent government fiscal restraint has been completely absent.

Conclusion:

The current market for Nvidia, mega cap stocks, and capitalization indexes appears poised for a generational decline commencing with a bubble bursting in Nvidia stock.

Equity market valuations are near all time highs and comparable to stock market bubbles in 1901, 1929, 1966-74, and 2000. The Fed Risk Premium model quantitatively illustrates that we are near all time high valuations with a premium of 0.35%. However, an economic decline or recession will surely undercut support for equities which are overvalued. Furthermore, a resurgence in inflation could push interest rates higher and also hurt the equity market.

MI2 Partners note that unemployment is crossing the 27 week moving average, a consistent indicator of an impending recession, which historically leads to a sharp decline in earnings and a bear market. Additionally, services inflation remains stubbornly high. This may be because the population is divided between wealthy equity owners and “the working class.” The wealthy have not begun to cut back on their foreign travel and self-indulgence, so a resurgence in inflation may manifest itself in the coming months driven by stubbornly high services inflation.

While a collapse in Nvidia is likely with its decline spilling over to mega caps and cap weighted indices in general, the severity and duration of the presumptive bear market will be greatly influenced by future rises in inflation and economic weakness.

October is historically known for market crashes, but September historically is the weakest month of the year. Over the coming months, we will carefully be monitoring inflation and economic strength as they could greatly impact how badly this parabolic spike in stock prices will correct when this current exuberance around AI exhausts itself.

Since market timing is hard, we urge a comprehensive review of your investments and consider shifting to a 25% stock, 25% bond, 25% commodity and 25% money market asset allocation. Most importantly, we see the 60% equity 40% bond asset allocation as largely overvalued and unsafe despite its good long term investment record. We have entered a new era with bubble valuations adue to the excessive and artificially low interest rates of the last fifteen years fashioned by the Federal Reserve in response to the Great Financial Crisis of 2008-2009.